BANK TREASURERS ATTEND A PASSOVER SEDER

The new year for the banking industry had a solid start, reporting in Q1 2025 that it grew earnings and kept balance sheets stable. In many respects, the message delivered during the bank earnings calls this month sounded like the message management sent for the last year: that the future is too difficult to predict amidst unprecedented persistent market volatility and economic uncertainty. According to the Fed's H.8 data, annual monthly loan growth is flat, while commercial and industrial (C&I) loan growth remains flat to negative. Management warned analysts this month that it was too early to tell and make projections about the direction of net revenues and capital returns for investors, much less the future of monetary policy, whether rates head higher, lower, or stay the same.

Uncertainty over tariffs, the direction of the Fed's monetary policy, and now uncertainty about whether Chair Powell will remain in his seat and who will succeed him when his term expires next year are the latest reasons management lists for keeping many of their commercial customers on the sidelines. Bank management expects these uncertainties to clear up before the summer when the tariffs and their effect on the economy will start to show up in the reported economic data or whether the White House will decide to roll back the tariffs before they take effect as it may seem to be doing here at the end of the month. Until then, the economy and markets could go in any direction, and bank treasurers are ready for any scenario. The CME FedWatch Monitor predicts three 25-basis point cuts to Fed funds by the Federal Open Market Committee (FOMC) before year-end, but Fed officials and bank treasurers both have doubts.

Regional and community banks cumulatively increased the balance of their deposits by 9%, to $5.7 trillion, since the failure of Silicon Valley Bank (SVB), Signature Bank (SBNY), and First Republic (FRC), a record level for the peer group. The increase was sufficient to fund loan growth over the same period, so the peer average for small bank loan-to-deposit ratios edged down from 84% to 82% this month. Net interest margins (NIM) and net interest income (NII) improved during the quarter despite the effect of rate cuts in Q4 2024, which narrowed the yield pick-up the industry earned on investment securities and loans rolling off and rolling on the balance sheet.

Bank management also credited positive earnings results to better-than-expected deposit repricing betas last quarter on business deposits and CDs, which helped offset the lower roll on/roll off yield pick up on earning assets, which, combined with disciplined expense controls, led to improved operating leverage. Meanwhile, bank treasurers remain vigilant about liquidity management, as commercial banks continued to hold $3.5 trillion in reserve deposits at the Fed, a level they have consistently maintained through 20 months of Quantitative Tightening (QT). During this time, the Fed shrank its System Open Market Account (SOMA) portfolio by $2.1 trillion to $6.7 trillion.

Bank treasurers are more conservative about liquidity management than they have been in previous rate cycles, and one reason for this could be the rise in digital payments and the development of tokenized money. FedNow, for example, is the Fed's new digital payment platform launched in July 2023 that business customers can use through their banks that are signed up to make instant payments. The Fed reported this month that the total value of payments made on FedNow in Q1 2025 equaled $49 billion, up from $31 million in Q1 2024 and $20 billion in Q4 2024. Leaving aside the opportunities for the banking system to leverage a digital payment service like FedNow, the industry continues to invest in artificial intelligence (AI) applications to improve efficiencies in routine processes. Bank treasurers are open to learning and adapting AI to enhance decision-making and risk management.

Six new banks were chartered last year, matching the number of new charters in 2023 but is down from 12 in 2022. The current rate environment, with a persistently flat to inverted yield curve in the front end, is one possible explanation for why today's banking environment is not hospitable to de novo banks. Another reason the industry points to is the regulatory burden on applicants and the time it takes for charter approval.

However, bank supervision appears poised to shift and take a less restrictive stance going forward with bank applications, as Fed Governor Bowman and the nominee to assume the role of Vice-chair of Supervision swore to Congress during her nomination testimony would be her mission to improve the operating landscape for regional and community banks. Large banks also expect some supervisory relief on the capital and liquidity ratio front, which they argue keeps them from supporting the Treasury market. The Fed proposed reducing the volatility of large bank capital requirements this month based on the annual stress test results.

The Bank Treasury Newsletter April 2025

Dear Bank Treasury Subscribers,

The Haggadah, read by participants at a Passover Seder, a dinner party conducted on the first night of the holiday, recounts the liberation of the Hebrew people from slavery. Passover is a liberation holiday. Though not exactly in the same vein as the White House's Liberation Day announced on April 2nd, there are some parallels between them.

For example, Passover and Liberation Day involve people getting to the promised land on foot. The Hebrews marched through the desert for 40 years to get where they were going. Presumably, the local mall would be the equivalent of the Promised Land for the American people who yearn to go there in a hurry to buy all the I Phones, television sets, Barbie dolls, Christmas ornaments, eggs, and tomatoes their presumably soon-to-be tariff-depreciated money could buy. Unfortunately, gas prices stubbornly hold, like facts, well above $2 at the pump, which means they will need to walk there, even if they could afford to pay for a car assembled here from suddenly more expensive parts made elsewhere.

And the parallels do not end there. The story behind both holidays involves a central character's churlish obstinacy who then relents, or sort of relents. For example, Moses, the leader of the Hebrews, came before Pharoah and demanded, "Let my people go." Initially unmoved, Pharoah, who some say had an orange complexion like the sun and whose people worshipped him as one, insisted that the Hebrews build him the biggest, most beautiful pyramid anyone had ever seen. Sternly, yet comically, he crossed his hands as he reportedly sang, "No, no, no, I will not let them go."

Similarly, the White House initially rejected pleas to pause the tariffs and ignored the Armageddon it wrought on America's equity and bond portfolios. "We are not looking at that," the Pharoah, er, president of the United States, told reporters earlier this month who asked whether it would be okay if the country stayed in slavery, or other words if the White House would kindly repeal, pause, or reconsider the tariffs. He reminded them that "sometimes you have to take your medicine," referencing the market's blindsided sell-off, which followed the country's liberation when news of the tariffs wiped trillions of dollars of the nation's hard-earned sweat savings off its collective brow overnight.

But Pharoah eventually relented and let the Hebrews go, who he said were being yippy. But then he changed his mind again, and he ran after them. The whole story came to a nail-biter at the Red Sea, which miraculously split at the last moment to let the Hebrews reach safety. But for a while there, the Hebrews had no idea whether they would make it to freedom or end up offed by Pharoah's murderous minions and left in the desert for the vultures.

Bank treasurers can easily relate to the situation in which the Hebrews found themselves. This month's message to equity investors is that the future is impossible to predict. It could go either way or any way, to be very honest. But bank treasurers will put their trust in—well, unlike the Hebrews, they probably do not put their faith in anything, but they naturally prepare for everything. Hard landings, soft landings, no landings, loan growth, or no loan growth. Rates up, down, or the same. Flat yield curves, inverted curves, and normal curve scenarios—whatever the market and the economy throw at them, they will be ready, Freddy. Bank treasurers are hoping for the best and can use a miracle.

Not feeling the liberated vibe just yet, bank treasurers are stressed out by their list of uncertainties, starting with the chances of recession, stagflation, and who knows what economic outcome in their immediate future. They hear that their tariff-related economic pain could be temporary but worry that April 2nd Liberation Day will go down in history, marking the end of civilization as they know it. Like the Hebrews, they might wish for a miracle now.

Miracles can be fleeting. The White House announced a tariff pause on April 5th, which must have sounded like one. But then it clarified that the pause would only last for 90 days. IPhone buyers must have been beside themselves. A day later, the White House clarified that the tariffs would exempt iPhones, which must have seemed gladdening until the next day when it further explained that the iPhone exemption would not last forever. Nothing lasts forever unless we are talking about uncertainty.

Why Is This Time Different?

The seder begins with a question. Why is this night different from all other nights? Traditionally, the youngest participant at the seder poses this question, a format bank treasurers understand very well, given that this is their approach to training the new kid they hired out of school as a junior analyst to sit on the treasury desk. Unless you ask questions, all the information will not inform you. Good answers require good questions.

Newbies have so much to learn. Between all the acronyms and the different products, the rules, the different examiners from the other agencies, how Fed funds work, what FedWire is, and so on and on. Plus, there is a lot of history they should know about. After all, they were in grade school during the GFC, maybe just learning to read and add two plus two. If they knew how things used to be, the newbies would better appreciate how things are now.

Maybe the odds that the economy ever finds itself facing the potential for ZIRP (Zero-Interest Rate Policy) and NIRP (Negative Interest Rate Policy) is next to nothing, but you never know what will happen next in the bank treasury world. A newbie’s education has no end, but it starts with a question. Why are bank treasurers different from all other corporate treasurers?

The path to wisdom begins with a question. Why are bank treasurers different from all other corporate treasurers? Because all corporate treasurers are a resource in their company, they are go-to experts for all questions about interest rates and the economy. They always have a ready opinion on the 2s-10s Treasury yield curve. All corporate treasurers maintain relations with other departments in their company and have working relationships outside the company with their counterparts in other companies and manage banking relationships. All corporate treasurers are, at their core, financial analysts who track their company’s key performance indicators (KPIs) and analyze their sensitivity in different scenarios.

But bank treasurers do all this and more. They track NIM and NII, net free funding, and know the difference between NIM and net interest spreads. They always look at risk and return in their investment portfolio and understand what positive and negative term premiums imply when considering extending the duration and by how much. They know everything: the intricacies of deposit repricing betas and the differences between branch and online deposit originations. Newbies can ask them anything and expect a ready answer.

While maintaining working relationships with the other department heads in the bank and trading Fed funds with bank counterparties, they always talk to their Wall Street coverage and coverage at their FHLB. They can pick up a phone and know who to call at the Fed’s discount window when needed. They are experts on where corporate rates might be and can hold forth on mortgage rates and Treasury rates.

Financial accounting helps answer questions about a financial entity’s economic health. Why are bank treasurers different from all other corporate treasurers? All corporate treasurers understand basic GAAP, know the income and expense accrual standards, and keep abreast of new developments at the Financial Accounting Standards Board (FASB). All corporate treasurers deal with auditors and practice good governance controls over their departments.

But bank treasurers do all this and more. Their balance sheets comprise interest-earning assets and interest-bearing liabilities, not property, plant, and equipment. Bank balance sheets get leveraged at multiples of what treasurers at companies in other industries would feel comfortable with balance sheet leverage. They spend a lot of time worrying about interest rate risk and how to model funds transfer pricing for loans and deposits. Because banks are short-option risk on both sides of the balance sheet, as assets can be prepaid or deposits withdrawn at the option of the counterparty, bank treasurers must be experts on option pricing and hedging, too.

Given the uncertain future, they need to think about hedging all the time. They need to understand the intricacies of multi-layer hedge accounting and effectiveness testing, at least enough to hold their own in a conversation with auditors. And they do not just talk to auditors. They speak to multiple bank examiners at the state and Federal level who want even more details on their hedging programs, asset-liability management, liquidity management, and interest rate risk management. They also are versed in capital and liquidity requirements, guidance, and best practices.

Bank treasurers know the most complex financial products and understand how markets work. They are traders, investment bankers, and asset managers. They are proficient in the latest technological advances in information systems, AI, and machine learning and are always looking for ways to improve the bank’s technological effectiveness and drive efficiency.

Today, the people in the bank treasury seat deal with some of the thorniest problems compared to what the average corporate treasurer working in other industries may see during their workday. They are dealing with historic liquidity-impairing unrealized losses in their bond portfolios, equal to $585 billion at year-end 2024, that complicate bank liquidity management and operating leverage and show no signs of meaningful recovery in the foreseeable future with the 10-year Treasury holding above 4.32%, mortgage rates hitting 6.9%, and rates for both threatening to go higher.

Even if he has failed so far after three years to bring inflation down back to the Fed’s 2% target, bank treasurers would hate to see Powell forcibly removed, as the White House threatened this month to do if the Fed did not bow its independence and lower the target range for Fed funds immediately. That scenario could make their problems with the fair value of their bond portfolios worse than they already are. The White House backpedaled, but market and economic uncertainty rose with the damage already done.

Bank treasurers know all about competition and unlevel playing fields that other corporate treasurers may not see in their respective industries. Banks compete with credit unions and are even getting bought by them, who they complain have an unfair advantage because they do not pay income taxes and enjoy less burdensome supervision from their regulator, the National Credit Union Administration (NCUA).

Banks also compete with unregulated nonbank companies, including Fintechs, and are even acquired by Fintechs which are getting their own bank charters. Today, bank treasurers see private equity hunting for consumer credit exposure in their traditional banking preserves, including consumer credit. Bank treasurers must consider all these factors when drafting their NIM and NII budgets because competition impacts pricing for their loans and deposits.

Another Question

Here is another question the newbie should ask at the Seder table or when they get back to their seat at the treasury desk: Why is this cycle different from all other cycles? Usually, economic cycles have their ups and downs, but this cycle is constantly up and down. Everything is so crazy this time that Chair Powell admitted in a speech he made to the Economic Club of Chicago on April 16th,

“We may find ourselves in the challenging scenario in which our dual-mandate goals are in tension. If that were to occur, we would consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close.”

Because as the CFO of FB told analysts,

“Obviously, the economy is kind of a wildcard.”

Indeed! Economic expansions and inflation are not supposed to continue after the Fed raises short-term rates by 525 basis points in 16 months. If rate hikes are supposed to be an antibiotic for an inflationary virus, the rate hike regimen the Fed put the economy through between March 2022 and July 2023 and holding them there at that level until September 2024 should have been enough to kill a horse, so to speak. Yield curves between the 3-month Treasury Bill and 5-year Treasury note are not supposed to remain deeply inverted for over two years. After the Fed cuts 100 basis points out of the target range for the Fed funds rate, the rest of the yield curve usually does not swing relatedly once steeper, then flatter, then inverted.

Because who knows? Because cycles generally do not run through a global pandemic, economists usually do not try to fit massive fiscal stimulus into their equations. The Fed never conducted monetary policy in the middle of a worldwide tariff war on a scale not seen since Smoot-Hawley that economists fear will have ruinous consequences for the U.S. and the global economy. Who knows what is still not in the data yet, at least not judging by the fact that the economy is still pumping out jobs and producing positive Gross Domestic Product (GDP) quarter after quarter since April 2020.

Unfortunately, long gone are the days when economic recessions were inventory-driven, as we were all taught in macroeconomics 101. There was a time when the supply of money mattered. Still, those days are even more ancient than the GFC, given the Fed’s commitment to maintain an abundant supply of reserves in the financial system well more than demand. After all, it is hard to die of thirst when swimming in as much liquidity as the Fed created in the system today.

There has never been a cycle where market and news volatility have been as wild as this. Bank treasurers are used to dealing with unknowns, but there has never been a time when there have been so many unknowns. Outcomes could go both ways, fifty-fifty, according to the president and CEO of a global bank who told analysts,

“We're trying to be as transparent as we can be about what the outcomes can be in terms of NII. But there are huge unknown…which… can go both ways. You can argue from the forward curve for many rate cuts…you can also argue there just won't be nearly the amount of rate cuts that are embedded in the forwards. And you see what's happened to the curve over the last couple of days little over the past couple of hours. The same holds true relative to what happens in terms of just loan balances. There are scenarios which could be both positive and negative for loan demand. It is a volatile time. It is a time of unknowns.”

It is impossible say, and as the chairman and CEO of a large regional bank told analysts,

“It's been a bit confusing for the last year or so.”

Confusion maybe goes back even longer..

Time For One More?

So, maybe one more question then. How much longer before we get back to the way everything used to be? And if the answer is another quarter, because that seems to be a consistent message from bank management to the market this month, what is so special about another quarter? The chairman and CEO of a global bank told analysts to wait another quarter, and after that, there may be fewer unknowns. Guessing the future, he said,

“Is almost impossible to answer. We look at all the cycles. And you know we prepare for a full range of outcomes. We're not -- I don't personally like predicting what the future is going to hold. But I do -- I pointed out over and over, there's a lot of issues out there. I think some of those issues, you are going to see them resolve for better or for worse in the next four months. So maybe when we're doing this call next quarter, we won't have to be guessing.”

He went on to say that this cycle is different from all other cycles because never has the fate of civilization been on the line,

“The most important thing to me is the Western world stays together economically when we get through all this and militarily to keep the world safe and free for democracy. That is the most important thing. I really almost don't care fundamentally about what the economy does in the next two quarters. That isn't that important. We'll get through that. We've had recessions before and all that. It's the ultimate outcome. What's the goal? How can we get there? And it's literally that. I mean the China issue is a major issue. I don't know how that's going to turn out.”

How Bank Treasurers Got Where They’ve Gotten

After the new kid finishes asking questions, everyone else around the seder table takes turns explaining the story of Passover, or how the Hebrews got to where they got to, or in other words, the whole business where they got enslaved and then came to be liberated. The story begins with a beginning that no one can seem to agree on. Was the beginning right after Covid, or was it after the GFC or the regional bank crisis two years ago? Was it since January this year when a new Administration took over in the White House? Was it on Liberation Day, or were the iterative corrections announced the days after?

Is the reason the job of bank treasurer is so hard because of the accounting rules on the investment portfolio and derivatives published in the 1990s? How far does one need to go back to get the full story into how bank treasury developed into the exciting mess it is today? Was it the fully phased-in version of Basel 3 in 2015 (what was supposed to be the “final” version) that caused all the problems we see today with the market dysfunction? Is it all because of the liquidity, leverage, and CET1 ratios? As the chairman and CEO of a global bank explained,

“Supplementary Leverage Ratio (SLR) alone isn't going to change that much for us. Really need reform across SLR, G-SIFI, CCAR, Basel III, and LCR, all of which have deep flaws in them to make a material change. And remember, it's not relief to the banks, it's relief to the markets…The reason why is…volatile markets, very wide spreads, and low liquidity in Treasuries, affects all other capital markets.”

Seders take a long time before the storytelling ends, and the feasting can begin. No one can agree on the beginning.

In the beginning, the ancestors of the Hebrews worshipped idols. Perhaps those were the first shibboleths. Why is funding with “brokered CDs” risky, which became an article of faith with bank supervisors since the 1980s? The story of how bank treasurers got here goes back to the GFC 17 years ago when the FDIC raised the cap on insured deposits to $250,000. Or maybe everything started 15 years ago when the total asset threshold for a SIFI was formalized at $50 billion under the Dodd-Frank Act, or 7 years ago when the current administration was in the White House before and signed the Economic Growth, Regulatory Relief and Consumer Protection Act (EGRRCPA) (aka, the Crapo Act) into law.

Why does the Fed dare not let reserves in the system fall below where they sit now, at $3.5 trillion? Because on September 15 and 16, 2019, the financial markets shuddered because of a sudden shortfall of reserve deposits. The Fed should have seen the circumstances coming, at least in retrospect, which included the settlement of a Treasury auction and tax payments on the same day. The shortfall caused the Secured Overnight Financing Rate (SPFR) to jump from 2.25% to 5.25%. The Fed had to come in to save the day and then decided to make an abundant reserve policy semi-permanent but said it might shrink it to just ample one day. Why does the Fed have a Reverse Repo (RRP) facility? The Fed’s indispensable tool, along with Interest on Reserve Balances (IORB), is to raise or lower the effective Fed funds rate because reserves exceed demand.

What was the genesis of the Fed’s Standing Repo (SRP) facility? The Fed needs it to calm the Treasury markets more efficiently by having counterparties preapproved and ready to borrow under it if needed. Why are bank examiners pushing banks to preposition collateral at the discount window? Because in their moment of need, SVB and Signature Bank were not prepared to borrow from it

In the beginning, the bank treasury landscape was more hospitable to banks than it is today. Banks were always opening branch doors and merging, obviously not anymore, of course, but back in the year 2000, over 100 new charters were granted, which was a low number. According to the FDIC, at the turn of the present century, there were 8,518 FDIC-insured institutions. Only 300 banks had total assets between $1 billion and $10 billion, and 79 had total assets over $10 billion. A large bank back then was considered any bank with total assets greater than $10 billion. As of year-end 2024, the FDIC reported that the,

“…total number of FDIC-insured institutions declined by 21 during the quarter to 4,517. Three banks were sold to credit unions, one bank closed voluntarily, and 18 institutions merged with other banks during the quarter. One bank opened and no banks failed.”

Flat and inverted yield curves do not make it easy for bank treasurers to make NIMs and NIIs or make for an inviting landscape for bank charter applicants. Bank charters plummeted since the GFC, but since 2010, the average yield spread between the 3-month Treasury Bill and 10-year Treasury note was 126 basis points, slightly narrower than the spread in the new millennium's first decade. De novo applications are cyclical, like the rate cycle and the bank treasury business. However, rate cycles do not explain why de novo applications fell off a cliff after the GFC and never recovered.

Maybe the weak de novo numbers have to do with the approval process the FDIC puts new applicants through since the GFC, which it tightened precisely to limit bank failures prevalent among de novo banks, as researchers from the FDIC discovered in 2016. The FDIC has 27 chapters in its application instructions for any equity investors thinking that commercial banking might be a good place to invest their money. There is a good reason the FDIC is so detailed. As they wrote,

“FDIC researchers also found that the failure rate of banks established between 2000 and 2008 was more than twice that of small established banks—consistent with previous research that found de novo banks to be susceptible to failure under adverse economic conditions. These findings underscore the importance of promoting the formation of new banks and establishing an effective application process and supervisory program that will ensure new banks adopt appropriate risk-management practices and enhance their prospects for long-term success.”

For the record, after the Crapo Act was passed in 2018, which was supposed to make it easier to apply for a bank charter, the number of new approvals rose from three to ten. It was an improvement, but these numbers were nothing close to the 150-plus new charters the industry saw on average before the GFC. Travis Hill, Acting Chairman of the Federal Deposit Insurance Corporation (FDIC), speaking this month, expected reforms to improve de novo formation, noting that the,

“…de novo rate has fallen off a cliff. From 1995 to 2007, the lowest number of new banks established in a year was 93. Going back a little further, in 1984, 412 new banks formed. Meanwhile, since the start of 2010, the total number of new banks formed over 15 years is 86, an average of less than 6 per year. Forty-four of those 86 opened in the four years between 2019 and 2022, a modest but meaningful increase largely attributable to reforms to the process and mindset put in place by Chairman McWilliams.”

Four Bank Treasurers

The Haggadah next relates the story of the four brothers, each with a distinct personality that is very different from one another. Bank treasurers will probably recognize themselves as one of them, at least in terms of their professional approach to their jobs. There were four bank treasurers: a wise one, a wicked one, a simple one, and one who did not know how to ask a question.

The wise bank treasurer asks bank examiners: What are the best practices for managing my bank’s interest rate and asset-liability management risk? Ever attentive to interest rate risk, the wise bank treasurer resisted pressure to move excess cash into bonds in 2021 when front-end rates hovered near 0% and MBS coupons were 200 basis points higher. The wise one did everything to hedge risk on the balance sheet and used new hedge accounting rules, such as multi-layer hedge accounting, to protect income against the risk that the Fed might need to raise rates faster and higher than anyone ever expected in those 0-lower bound days in 2020 and 2021.

The wise bank treasurer understands that hedging comes at a cost in the short term, but whose perspective is long-term. Wise bank treasurers remain vigilant about risk management and want to know how Eris SOFR swap futures (one of our corporate sponsors) can offer economies on hedging costs. The wise one is always up to date on technology and actively seeks ways to include AI in decision-making and risk strategy, which Straterix (another one of our corporate sponsors) would be happy to explain to any wise bank treasurer who is interested, and what wise bank treasurer would not be interested in finding ways to do their job better?

Bank treasurers must find ways to incorporate new AI, machine learning, and generative AI technologies in treasury desk functions, which will not replace them but will help them make better, faster, and more efficient decisions. It might make it possible for bank treasurers to get a break occasionally, given that all the volatility in the market keeps them up at night. As the CFO of a large regional bank on the East Coast told analysts,

“Our ALCO team and treasury has been working hard because rates keep changing and the curve keeps changing. So, it's a very dynamic environment, for sure.”

The technology’s power is to let one bank treasurer leverage it as if they had a department many multiples of the typical treasury department staff headcount. As Fed governor and former Vice-Chair of Supervision Michael Barr said this month,

“Gen AI-based analytic tools can build on existing algorithmic trading capabilities by harnessing an enormous knowledge base in both the public and private domains. These enhancements have the potential to enable decisions that are faster and more informed.”

The wise bank treasurer probably holds a lot of cash on the Fed’s balance sheet, even if there are better opportunities in a 3-year duration mortgage product. You can see it in the Fed’s H.8 numbers (Figure 1) for cash assets which continue to hold above average relative to total assets.

All corporate treasurers are sitting on more cash, even the ones who do not work at a bank. Eventually, the money will be put to work when economic conditions become more hospitable. But as for now? The chairman and CEO of a leading asset management company told analysts,

“We're seeing an elevated increase in April, which is an unusual time to see elevated increases in cash. We had $20 billion in inflows this month alone in cash. But let's be clear, there's over $12 trillion in money market funds. So, there is a huge reserve of money that will be put to work in the future. We're having a lot of conversations related to fixed income. And you think about as a yield curve steepens and we are a big believer of the yield curve is going to continue to steepen, in the coming months, as the yield curve continues to steepen, we're probably going to see more people extend out. And it represents more opportunities.”

Wise bank treasurers would have a broad menu of liquidity options and a channel into R&T Deposit Solutions and StoneCastle Partners, two of our other corporate sponsors, to help meet funding management objectives. Wise bank treasurers would regularly test credit lines with the discount window and the FHLB and keep procedures up to date. Governance is their middle name.

A wise bank treasurer, appreciating the cost of using a Futures Commission Merchant (FCM) owned by a large bank, would research business opportunities with a nonbank FCM, such as RJO Brien, yet another of our corporate sponsors. If a treasurer were wise and looking for an economical way to manage their residential whole loan portfolio, they would sign up for ORSNN, a low-cost platform for buyers and sellers of residential whole loans to connect, value, and swap loans peer to peer.

Wicked bank treasurers do not believe the rules apply to them and frequently run afoul of best practice. They loaded up their bond portfolios in 2020 and 2021 with 2% and 3% MBS and refused to hedge interest rate risk, preferring to just throw everything into held-to-maturity, where they carried the bonds at historical cost and did not report fair value. Wicked bank treasurers focus on short-term opportunities and ignore the long-term consequences. Wicked bank treasurers probably got paid for their 2021 NII and NIM management, then left it to their successors to clean up after the mess they made.

Figure 1: Cash Assets, Percent Total Assets, All Commercial Banks

Worse than what the wicked bank treasurer did in the bond portfolio was the total lack of preparation for stress scenarios and how they would impact the liability side of the balance sheet. The wicked bank treasurer is lax on governance, lazy about testing contingency funding under different stress scenarios, and as bank examiners wrote when they slapped down SVB’s liquidity rating to conditional in August 2022,

“[These] material financial weaknesses in practices or capabilities may place the Firm’s prospects for remaining safe and sound through a range of conditions at risk if not resolved in a timely manner. Key liquidity risk management deficiencies, identified in the Liquidity Target Examination supervisory letter issued on November 2, 2021, include internal liquidity stress testing design weaknesses, such as the lack of deposit segmentation, the lack of differentiation between market and idiosyncratic risk scenarios, and the lack of testing of the firm’s contingency funding plan. The examination also identified a lack of effective challenge by the second line independent risk function over the first line treasury business unit.”

The simple bank treasurer asks: what’s happening dude? And nothing against the simple bank treasurer, because most of them work at real small, simple community banks, probably with total assets under $500 million. The bank has its long-time depositors and its business borrowers who the simple bank treasurer will mingle with at the rotary club. The bank has a few branches which are all in the same town, and there is nothing too complicated about setting loan and deposit rates. Everything is just going to be SOFR plus or minus something, and usually the only reason the bank does any business at all in town is because the coffee it serves in its branches is better than the coffee served by the town’s credit union.

Simple bank treasurers are 6-3-5 people. They lend money at 6%, take in deposits at 3%, and are on the golf course by 5 PM to play a few holes. Sure, they took all the bank treasury classes on line, they get the whole business with funds transfer pricing, but the bank does not really need that. They learned about options and swaps, but the board looks askance on swaps and other derivatives to hedge risk or would even consider a lower cost option such as an Eris SOFR swap futures contract. Derivatives are the devil is the attitude.

Their bank’s investment portfolio is simple, and there is no swinging for the fences. You won’t see CLOs or other types of credit instruments in the bank’s bond portfolio. If there is going to be anything driving NIMs and NIIs it will be plain old taking deposits and making loans.

The problem with simple is that simple does not cut it anymore, especially if a bank does not want to be one of the acquired banks next year and merged out of existence. Chair Powell said he thought the position of Vice-Chair of Supervision was unnecessary, a role that Fed Governor Michael Barr vacated this year. Nevertheless, the soon-to-be confirmed new Vice Chair of Supervision, Michelle Bowman, told Senators at her confirmation hearing this month,

“To remain viable and competitive, banks must be able to consider new technologies that can improve products and services, and lower costs.”

Simple bank treasurers make simple assumptions about interest rate risk. Still, risks are not always straightforward, especially in the current environment where it is even odds that the next move by the Fed is a rate hike or a rate cut. And even if the future was not as uncertain as it is today, what bank treasurer would not want to have a way to track every single cashflow on the balance sheet going in or out, the ability to design customized scenarios, drill down to granular levels on deposits, and conduct what-if analysis?

Even a simple bank treasurer at a simple bank with total assets under $500 million would want that kind of thing, provided it can come at a straightforward price. Hedgehog, another of our corporate sponsors, has that offering for the bank treasurer who wants the product but has a simple budget.

Finally, for the bank treasurer who does not know how to ask questions, here are some of the ones other bank treasurers are asking or should be asking:

How should tariffs change my outlook on interest rates? Why did the Fed cut the QT cap on Treasurys from $25 billion to $5 billion last month? Does this mean QT is ending soon? Is the Fed’s monetary policy still effective in controlling the economy, or has the Fed’s power declined since the GFC given that its rate hikes did not bring down inflation after 3 years to target? What is the connection between the Fed’s balance sheet and bank deposits, because if the Fed’s balance sheet is shrinking, why are bank deposits still growing?

Will tokenization be good or bad for banks? Will it change how bank treasurers manage liquidity or model the behavior of core depositors? When will the Fed increase the hours of FedWire to 22x7, and what is the latest on FedNow? The Fed reported that total settled trades on that platform at the end of Q1 2025 equaled $49 billion, up from $31 million in Q1 2024. Will Congress raise the cap on insured deposits to over $250,000, considering that the cap was established in 2010 when bank deposits equaled $8 trillion and today equal $18 trillion, especially considering today’s total deposit number includes $7 trillion of uninsured deposits?

The Plagues

The Seder follows the four sons with a recitation of the plagues, which, according to tradition, beat a disruptive path through Pharoah’s kingdom to coerce him into manumitting the Hebrews. Bank treasurers have seen their fair share of plagues in recent years. Maybe not the blood, frogs, lice, wild animals, pestilence, boils, hail, locusts, darkness, and the death of the first-born variety of plague, but still every bit as disruptive to the banking landscape.

Start with the plague of record negative AOCI, the failure of three large regional banks in 2023 that set off a tidal deposit outflow from small banks to big banks, the plague of flat to inverted yield curves that do not help bank treasurers trying to generate NIM and NII, and the plague of market volatility that never ends. Maybe bank treasurers at large banks can make money in these markets, as the chair and CEO of a GSIB explained,

“Volatility leads to bigger bid-ask spread that all things being equal is better. And it leads sometimes to higher volumes. So you've seen higher volumes in FX and interest rate swaps, and Treasuries. That's better. But sometimes that kind of volatility leads to very low volumes. Like you see in DCM today, when you don't have these bond deals and where you have less trading.”

However, volatility is a plague for the rest of the financial system and economy, on the retail or business side of a bank’s balance sheet, in loans and deposits. It is like the after tremors following an earthquake rattling the survivors and keeping them in the bunkers: decisions about whether to buy or sell a new home, start a new business, expand, or partner up with a competitor in a merger and acquisition, all put off until the tremors die down. The trauma is not just disruptive; it is potentially destructive with long-term consequences beyond just business deferred for the short term. There is just so long that participants in the financial system can go around holding their breath and waiting for some quiet.

There were more plagues. There was the plague of uncertainty, the plague of a federal deficit out of control. There was the plague of growing doubts about the dollar’s status as a reserve currency in the post-liberation days ahead. And perhaps finally, there was the plague of the tariffs, which threatened to upend the economy and the world order, but whose potential damage is too difficult to predict.

Dayenu-It Would Have Been Enough

At this point in the Seder, the Haggadah directs participants still wondering when they can eat dinner to focus on the good things that happened to the Hebrews after they escaped Pharoah. Despite all the headwinds they went through in recent years, bank treasurers have had several lucky breaks of their own, and they can start by thanking the Fed for many of them. From a bank treasurer’s perspective, it would have been enough if just one of these things had happened. It would have been enough, or in the language of the Haggadah, if just one of these things happened, it would have been “Dayenu.”

Dayenu! Had the Fed just created the Bank Term Funding Program as a nifty contingency source of funding for suddenly deposit-strapped regional and community banks, which it ran from its discount window, but did not make the terms so generous as to provide bank treasurers with an easy money-making arbitrage, it would have been enough.

If the Fed had only gone 25 basis points at the FOMC’s September meeting last year instead of 50 basis points, it would have been enough to help bank treasurers manage NIM and grow NII.

If the Fed had kept an ample level of reserve deposits and not abundant reserves, if, say, reserves equaled $3.0 trillion instead of $3.5 trillion; it probably would have been enough to avoid another panic in the repo market as happened in September 2019, especially given that the Fed can turn to its SRP to calm the markets.

If the Fed caused the economy to slip into a mild recession or a soft landing, instead of no landing, it would have been enough.

If the tide that drew deposits from small to large banks would have only reversed and balances returned to their pre-SVB levels of $5.2 trillion in February 2023 instead of a record $5.7 trillion as the balance of deposits equaled this month, it would have been enough. It would have been enough because the loan-to-deposit ratio for small banks would then have equaled 85% instead of 82% as it does today, using the Fed’s H.8 data series comparing the current balance of loans for the small bank peer group to the average balance of deposits in February 2023. Even at 85%, the average small bank ratio of loans to deposits is still below 87%, the peer group’s loan-to-deposit ratio for the past 30 years.

Seder Songs

Finally, Seder participants get down to feasting on multiple courses involving matzah, which has disastrous gastrointestinal consequences for them, which they will only realize the following day. But after dinner, the Seder concludes with a few fun counting songs. Tired and ready to go to bed, bank treasurers would want to stay and sing their version of these Seder songs. For example, the famous song “Who Knows One? I Know One” could go like this:

Who knows one? I know one. One is the year left to Chair Powell’s term as Fed chair if he makes it that long before he goes back to just being another Fed governor whose term ends in 2028. Who knows two? Two is the Fed’s target for inflation, which remains elusive and is now in danger of getting further away. Who knows three? Three are the rate cuts the market consensus still believes will happen before the end of this year, according to the CME FedWatch monitor. Who knows four? Four is the handle on short and long Treasurys, with the 3-month T-Bill holding at 4.3% and the 10-year at 4.4%. Who knows five? Five is the new $5 billion monthly cap the Fed set last month for run-off from its SOMA Treasury portfolio.

Who knows six? Six are the six new commercial banks chartered by the FDIC last year. Who knows seven? Seven governors of the Federal Reserve who, by law, cannot serve for more than 14 years. Who knows eight? Eight are the permanent voting members of the FOMC, consisting of the seven Fed governors and the president of the New York Fed. Who knows nine? Nine is for the F-9 key that every bank treasurer wished they had to solve their balance sheet issues instantly.

Who knows ten? Ten is obviously the 10-year Treasury. What else would it be? Who knows eleven? Eleven is the number of FHLBs currently operating and providing $667 billion in advances to insured institutions, and by law, cannot number less than eight. Who knows twelve? Twelve are the number of Federal Reserve banks and the voting members of the FOMC. Finally, who knows thirteen? Thirteen is the number of weeks in a 3-month T-Bill, which still pays investors 4.3% when the average national deposit rate, according to FRED, for a 3-month insured CD with a balance under $100,000 pays just 1.4%.

One is the year left on Powell’s term, two is the 2% target inflation rate, three are the three 25 basis-point rate cuts bank treasurers expect this year, four is the handle on short and long Treasurys, five is the new $5 billion monthly cap the Fed set for run-off from its SOMA portfolio of Treasurys, six are the six new commercial banks chartered by the FDIC last year, seven are the seven governors of the Federal Reserve, eight are the permanent voting members of the FOMC, nine is for the F-9 key that every bank treasurer wished they had, ten is the 10-year Treasury, eleven are the operating FHLBs, twelve are the regional Fed reserve banks, and thirteen is the number of weeks in a newly issued T-Bill.

The last song that closes the Seder concerns a little lamb that someone’s father bought, which sets off a list of consequences involving getting eaten by a cat and the cat getting bit by a dog, which gets hit by a stick. The song connects dots one after another until the end when everything is consolidated. The song is called, “Chad Gadya,” meaning one little lamb.

Bank treasurers might sing this version of the Chad Gadya before they pack up and go home for the night, given the likelihood that bank consolidations revs up this year. Indeed, bank supervisors just approved a major bank merger application that was languishing in their inbox for over a year:

One small community bank, one small community bank: There was once a small community bank in a small town that served great coffee in its branches. One small community bank, one small community bank. Now, a slightly larger community bank bought the small community bank and continued to serve the bank’s coffee in all its branches, one small community bank, and one small community bank. Then the newly combined bank went and did a merger of equals with another similar-sized community bank to become one of the top 3 bank networks in the state, one small community bank, one small community bank.

Now, this new bank drew the attention of a mid-sized credit union operating in its region, which liked the opportunity to expand in the state, with one small community bank one small community bank. The mid-sized and now much bigger credit union which does not pay taxes and has an unfair advantage against like-sized commercial bank charters, merges with another large credit union, one small community bank, one small community bank.

These M&A iterations continue until one day; the successor large credit union sells to a private-equity-backed Fintech, one small community bank, one small community bank. But unfortunately for the small town, the Fintech decided to shut down all the town’s bank branches that served the great coffee, one small community bank, one small community bank.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2025, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

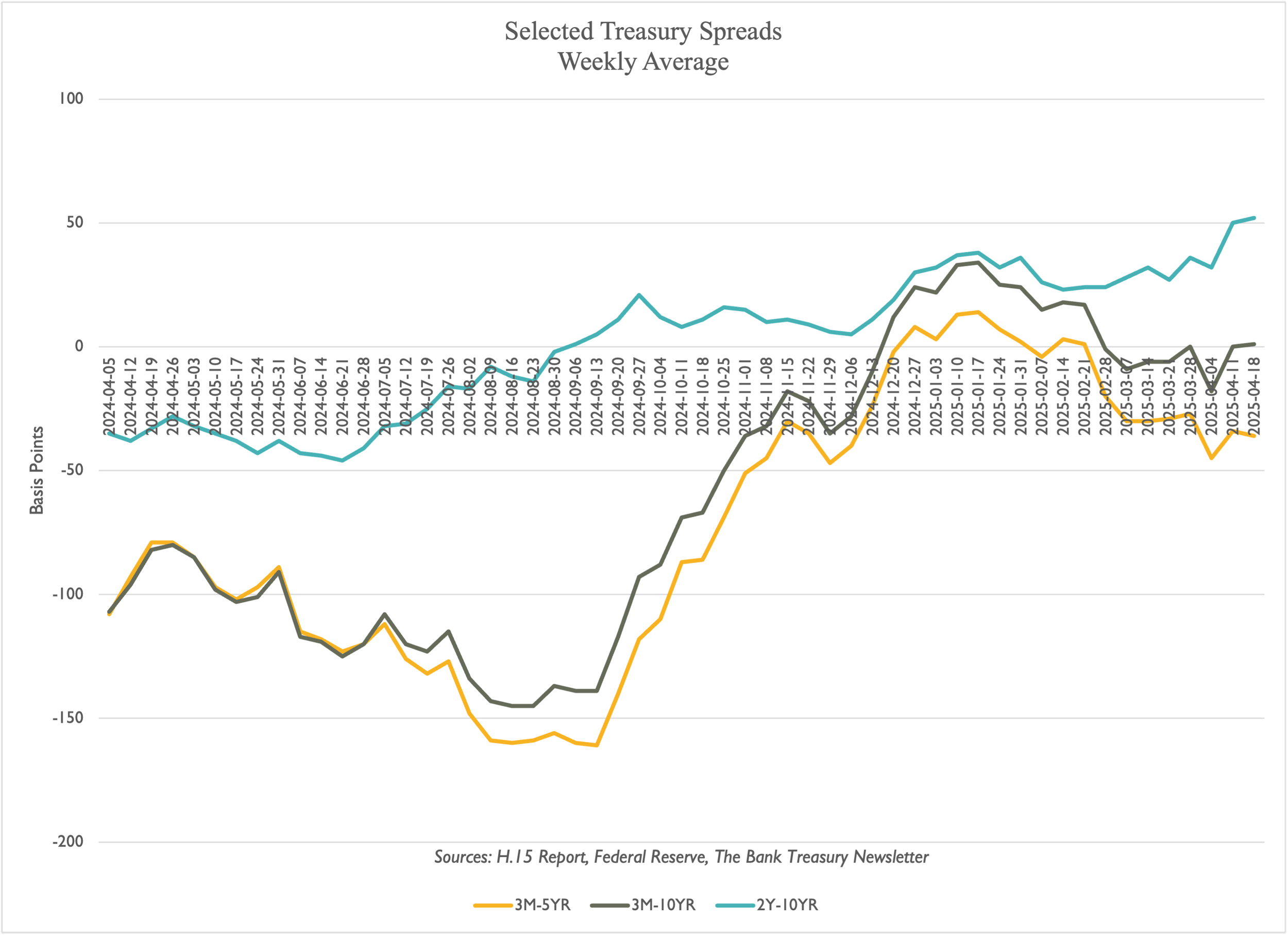

The interest rate picture is difficult to interpret, whether the direction the different benchmarks are going in portends good or bad news about the bank treasury landscape. Short-term rates are high, at least relatively so, judging by the 4.3% prevailing Fed funds rate and comparing it to the 1.8% rate Fed funds have averaged going back more than 30 years (Slide 1). However, interest rate trends do not help clarify the economic path ahead. The 2s-10s yield curve (Slide 2) returned to a positive slope last September when the Fed cut rates and continued to steepen this month, which some economists might say means the economic picture is brightening. Yet, the 3-month-5-year and 3-month-10-year Treasury spreads tell a different story. Both finally returned to a positive slope last January after two years in negative territory but reversed course a month later. The 3-month-5-year spread is back to being inverted today, and the 3-month-10-year spread is flat .

So, are rates going up, down, or remaining the same? Who knows, but to some degree, when the Fed stopped hiking rates in July 2023, it took pressure off bank funding costs, as bank treasurers were suddenly able to reprice deposit rates lower (Slide 3) and continued to do so last month. Loan demand is off, as borrowers sit on the sidelines until all the uncertainty clears (Slide 4). For community banks, that relief has translated into a lower ratio of loans to deposits (Slide 5) .

FedNow is an instant payment platform like Venmo and Zelle, except that the Fed runs it and allows businesses to make large dollar payments. The Fed launched it in July 2023 after the failure of Silicon Valley, Signature, and First Republic when the industry was still reeling from the trauma of watching depositors run against large banks seemingly overnight. The take-up of the service was initially slow, and quarterly payments totaled a few million dollars in the first few quarters. But in Q3 2024 and since then, FedNow has become an example of “build it, they will come,” as total payments last quarter equaled nearly $50 billion (Slide 6). This number compares to the total payments originated over FedWire (Slide 7), which equaled $285 billion in Q1 2025 .

Tariff turmoil caused the US dollar to fall in exchange markets, such as against the Euro (Slide 8). There is a lot at stake that the tariffs have put at risk. For example, world merchandise exports equaled $24 trillion, led by Asian markets including China and Vietnam (Slide 9).

It is raising, if not showering, uncertainty in April, as the Economic Policy Uncertainty Index, a data series that goes back to 1985, hit a record (Slide 10) this month, beating out the uncertainty caused by Covid and dwarfing all other previous periods of uncertainty, including the Global Financial Crisis, 9/11, the Iraq War, 9/11, and Y2K.

Fed Funds Rate Direction Unknown

Yield Curve Tell Different Stories

Consumer Time Deposit Funding Gets Cheaper

C&I Loan Growth Flattens Out

Bank Balance Sheet Liquidity Stable

FedNow Takes Off

Most Payment Activity Runs Through FedWire

US Dollar Sells Off This Month

World Trade: A Lot To Lose

Uncertainty Index Hit A Record