BANK TREASURERS INTERVIEW JAY AI

The Federal Open Market Committee (FOMC) voted to maintain a "wait and see" approach for rate cuts in 2025, keeping the target range for the Fed funds rate between 4.25% and 4.50%. The financial markets widely expected this outcome given the solid economic readings that continue this year and despite concerns that new trade policies might derail the economy later this year. The Atlanta Fed's GDP Now monitor projected a negative print for Q1 2025, equal to -1.8%, while the FOMC's latest dot plot projected slower Gross Domestic Product (GDP) growth in 2025 but no recession. Bank executives observed that businesses are delaying investments because of tariff-related uncertainty and relayed their concern that Federal worker layoffs will begin to take their toll on the economy. Following the release of the FOMC statement on March 19th, the Treasury yield curve remained unchanged, the spread between the 3-month and the 5-year slightly inverted, and the spread between the 2-year and the 10-year somewhat positive. Rates on mortgage-backed securities (MBS) were also steady after the meeting.

The FOMC also announced that it would lower the pace of Quantitative Tightening (QT) for Treasurys from $25 billion to $5 billion monthly. Bank reserve deposits, which remain the lifeblood of the financial system and, if there were to be a shortfall, would bring the Treasury trading market to a halt, equal $3.5 trillion, a level that has remained constant since QT began in June 2022 thanks to the balances in the Fed's Reverse Repo Facility (RRP) and more recently, the Treasury General Account (TGA) which absorbed most of the outflow from the System Open Market Account (SOMA) portfolio. However, the balances of the RRP and TGA are now close to their respective floors, and thus, QT will begin to put downward pressure directly on the level of reserve deposits as it continues. Cutting the monthly cap on Treasurys will help mitigate the effects of QT. The Fed kept the cap on MBS unchanged at $35 billion, but only $15 billion runs off monthly in its MBS portfolio, so combined QT will reduce reserve deposits by $20 billion a month. Even at this reduced rate, as the Fed remains committed to maintaining reserve deposits at an abundant level, bank treasurers should expect the Fed to end QT in due course.

The bank regulatory pendulum is already swinging towards a more relaxed regime than in recent years. Chairman Jerome Powell has all but committed to "re-calibrating" the Basel 3 Supplementary Leverage Ratio (SLR) that large banks contend is holding them back from investment in the Treasury's projected debt issuance this year, affirmed his belief that the large banks are already well-capitalized, and hinted that when regulatory agencies eventually release a new draft proposal for the Basel 3 Endgame that the banks that are in scope will not need to raise additional capital, even though Category III and IV banks will need to include Accumulated Other Comprehensive Income (AOCI) in their regulatory calculation. According to the latest SIFMA data, average daily trading volumes in Treasurys reached over $1 trillion last month. The White House nominated Fed Governor Michelle Bowman as the Fed's new Vice-Chair of Supervision. She has been a vocal critic of the push under the former Vice-Chair to raise capital and liquidity requirements for Category III and IV banks. Other proposals she has expressed reservations include assessing them with a long-term debt requirement and possibly a short-term Liquidity Coverage Ratio requirement.

Under Travis Hill, the acting chair of the FDIC, in the last month, the FDIC withdrew a proposed rule on brokered deposits, published in August 2024, in response to Synapse's bankruptcy in April 2024. Synapse was a fintech that regional banks were using to source deposits, and when it went dark, it froze deposit accounts introduced to the banks through its platform. FDIC restrictions on brokered deposits usually only impact banks that fail to meet the threshold for well-capitalized, but the proposal's definition of brokered and resulting reporting requirements would have affected any institution that used fintech channels to source deposits, imposing a significant compliance expense. According to FDIC data, brokered deposits equaled $1.2 trillion at the end of 2024 or 6% of total deposits.

The FDIC also withdrew a proposal on board governance published in October 2023. Like its brokered CD proposal, the FDIC proposed it in response to a bad outcome, which in the case of the governance proposal was the failure of Silicon Valley Bank’s (SVB) board to oversee management when the bank failed. The requirements in the proposal would have impacted banks with total assets over $10 billion. Industry lobbyists complained that it would have increased the bank board's difficulty in recruiting new members. The FDIC also proposed to rescind a policy on bank mergers and acquisitions (M&A), which it had finalized only last year because it said that the policy statement added "considerable uncertainty to the merger application process." More straightforward rules around M&A may encourage bank buyers, but when talking to analysts, bank management cautions that it will not help increase the supply of willing bank sellers. Nevertheless, according to the latest FDIC data, there were 4,487 insured institutions at the end of 2024, down 30 banks lost through M&A in the last quarter.

Arguing that the information was unnecessary or too sensitive to disclose, the acting chairman also announced last month that the FDIC would no longer disclose the aggregate total assets of its list of problem banks. At the end of 2024, there were 66 banks on the problem list, which includes banks with a bank supervisory composite ratings below a "3." The number of problem banks remain near historic lows going back 40 years. The rationale cited for not disclosing total assets, a number it had been disclosing since 1990, was that it either helped the public to identify financially distressed banks that went on the list or incorrectly identified perfectly healthy banks. Notably, as the acting chairman said in his statement, a bank could be downgraded to a "4" or even a "5" due to problems with management, and the rating change could be unrelated to its financial condition. Chairman Powell told Congress when he testified last month that he remains committed to modernizing and improving the discount window but also acknowledged the long-standing stigma issues that may dissuade a bank treasurer from using the facility in a liquidity stress scenario, who would turn instead to the Federal Home Loan Banks (FHLB) for an advance.

Bank investment in artificial intelligence technologies continues to grow. Industry executives view it as potentially transformative and a vehicle for driving operational efficiencies, leveling the competitive playing field in new markets, and improving risk management decision-making. Straterix, one of this newsletter's corporate sponsors, developed a scenario risk calculator that bank treasurers can use to improve decision-making around credit, liquidity, asset-liability management, and interest rate risk. The software uses machine learning technology and helps bank managers discover hidden sensitivities in their balance sheets that may only manifest themselves under specific scenarios. It also helps calculate the probabilities of different scenarios happening. While it cannot predict outcomes, it can provide insight into why banks such as SVB, Signature Bank, and First Republic failed, even though neither regulators nor market analysts ever imagined the possibility that they would have failed.

The Bank Treasury Newsletter-March 2025

Dear Bank Treasury Subscribers,

Meet Jay AI, the newest member of the newsletter’s editorial staff. Jay AI is an artificial intelligence (AI) bot, which, for our subscribers who are not up on the lingo, is short for robot, a shorthand that entered the lexicon about 25 years ago. Our subscribers may remember Ben AI, Jay AI’s predecessor, who our IT staff developed in 2021 with the help of ChatGPT and the website Character.ai. Since then, the technology has vastly improved, and no offense meant to Ben AI, but Jay AI is just light years better.

We all had such high hopes for Ben AI, or Ben as our office staff liked to call him—er, it. Ben was the next best thing to having a real live Fed chairman work at the newsletter, given its Ben Bernanke profile, the former chairman of the Fed from 2006 to 2014. Ben was going to be our 24/7 research assistant. With the proper training and supervision, everyone hoped it could one day even write research for the newsletter. The staff was excited to have Ben join our weekly staff meetings. If nothing else, like Amazon's Alexa, Ben could order office supplies when needed and play tunes for our after-work staff parties organized around that new barbecue grill your editor-in-chief (EIC) bought for the office last summer.

Unfortunately, nothing quite worked out the way we had expected. For starters, Ben believed that the year was 1980 which was when Ben’s human counterpart began teaching economics at Stanford. And, it may have been a bot, but it seemed to have a weird personality. When Ben picked songs from the Top 100 list from 1980, it was as if Ben were trolling the staff. It kept choosing songs with titles such as "Another One Bites The Dust," "Just Another Day in Paradise," "Heartache Tonight," and "Upside Down," which given their obvious bank treasury overtones, felt a little disturbing and certainly not helpful for our staff writers who were looking to unwind after a stressful day trying to make sense of all the volatility and upheaval in the bank treasury world. So, staff began to complain.

But more problematically, because it believed it was the year 1980, even though it was 2021, it insisted that the Fed funds rate was over 20% and banged the table, insisting that bank treasurers should just back up the truck and buy up all the MBS they could find. No number of "reminders" that we were in the 21st century seemed to help keep Ben stay oriented in the here and now or appreciate that the bonds that bank treasurers were buying in 2021 came with coupon rates nowhere near the record highs bank treasurers were getting in the Treasury market in 1980. The coupons in 2021 were at record lows. To top it all off, Ben could not even get facts straight, as the first Fannie Mae MBS did not hit the market until 1981, not 1980 when the rate on a 30-year residential mortgage loan peaked at over 18%.

Perhaps it is fair to say that our bot was supposed to sound like a Fed chair, and Fed chairs probably would not be picked for the job because they are good at managing bank treasury portfolios. That is possible. But even that aside, Ben was just as confused about monetary policy as it was about investment strategy. If asked in 2021 whether the Fed would raise rates, it would respond with arguments about why the next move would have to be a cut, unaware that rates were already at the 0-lower bound.

Ben was behind on the day's news, which is disappointing for a technology that is supposed to think faster than any human can and at least should be up to date on basic facts. Admittedly, facts have been changing rapidly for so long now. A year ago, bank treasurers still thought there was going to be a recession, then there was going to be a soft landing. There might be no landing, but then we returned to the recession scenario because of tariffs, and everything was wait and see.

Data has been everywhere. Inflation is up, it is up more, then no, wait, it is down. The markets are selling off, but now they are rallying. The 3-month-5-year Treasury yield was steeply inverted, then flattened, then it got a little positive-sloped, and now it is reinverted again. There is war, there is the price of eggs, the stock market is up, now it is mixed, and now it is down. The only thing unchanged is that the mortgage business is still weak. On and on welcome to the world of bank treasury, where the news never stops, and the news is never good. It is no wonder bank treasurers do not want to leave their bunkers.

That is why Ben should have been great. Ben could have shown some initiative for all the time and money the IT staff put into developing "him." Okay, maybe initiative is a human trait, but maybe Ben could have been at least programmed to send out daily updates on the latest news and data, perhaps even summarize it with some graphs. Who knows. But even just basic stuff it could not manage. Watch what happens when I ask Jay AI for an update:

EIC: Mr. Chairman.

Jay AI: Hi, call me Jay.

EIC: Okay, Jay. Thank you. First question, what are the latest key economic numbers that bank treasurers should be thinking about?

Jay AI: The Fed looks at a wide range of indicators, but GDP expanded at a 2.3% annual rate in the fourth quarter of last year, extending a period of consistent growth that has been supported by resilient consumer spending. Many indicators show that the labor market is solid and broadly in balance. The jobs report released this month showed employers added 151,000 jobs to payrolls in February and the unemployment rate was 4.1% last month. Personal Consumption Expenditures (PCE) prices rose 2.5% over the 12 months ending in January and that, excluding the volatile food and energy categories, core PCE prices rose 2.6%.

EIC: That is very helpful, Jay. Thank you.

Jay is night and day compared to Ben. Nothing in the question posed above was all that hard to answer. Jay just had to check the web. However, I asked Ben to browse the internet to find answers to staff questions at our weekly meetings, and it said that it does not do browsing, or wash windows for that matter. To top it all off, when I tried to interview Ben for insights about Ben Bernanke for the newsletter, it suggested that I should ask Ben Bernanke directly.

Businesses Warm Up to AI

Regrettably, after a few frustrating months trying to find ways to work with Ben, our staff concluded that he, it, them was not working out and needed to be deleted…er…turned off…er…let go. Ironically, in retrospect, this was precisely around the time that AI’s growth story began to take off in earnest, no longer just a bot oddity but increasingly seen by professionals as an indispensable tool for risk management, one that bank treasurers can use as they navigate through the most uncertain times in financial markets in modern times. According to a new study by McKinsey, businesses that used AI in at least one business function last year increased from 20% to 78% of the organizations it surveyed from 2017 to July 2024 (Figure 1).

All bank treasurers, whether at large, medium-sized, or small banks, whether at a bank or a credit union, ultimately swim in the same ocean or breathe the same air. Take your pick of metaphors. Rates going up or down, economy headed to a soft landing, no landing, or a tariff-fueled crash landing, inverted and positively-sloped yield curves all matter to every one of our subscribers.

But it all matters differently depending on the specific balance sheets that each bank treasurer manages, whether the balance sheet is naturally liability-sensitive, asset-sensitive, or neutral. AI can process information at light speed, but then it can instantly synthesize that information to fit the specifics of each balance sheet. It will never replace human bank treasurers as decision-makers, but it is an ideal tool for decision-making tailored to each institution’s circumstances. The CFO for a regional bank in the southeast explained how bank managers are working with AI,

“AI is one of those things that's moving so quick. You can hardly keep up…The biggest thing about AI…is a person still must be involved. You can't just set up a chat bot. You can't just…let it run. You still got to validate it, you still got to test it, you still got to look at what's happening.”

So, I asked Jay if it agreed:

EIC: Jay, will AI replace a human bank treasurer one day?

Jay AI: Hi, call me Jay. It's true that artificial intelligence has made rapid strides in recent years. However, as emphasized in the quote, humans remain critical in the process. AI systems require human oversight and validation. It's not a matter of replacing human decision-makers entirely, but rather harnessing AI to augment and support human decision-making. The human element is still necessary to verify the output of AI systems, ensure ethical use, and make final decisions. So, while AI can assist in various tasks and decision-making processes, it will likely not fully replace human decision-makers in the foreseeable future.

The foreseeable future phrasing at the end of Jay’s answer caught me, but I moved on to ask:

EIC: Jay, last month, the former Vice-Chair of Supervision, Michael Barr said he believed that both the banks and the Fed need to invest in AI. Let me read this quote from from the speech he made last month to the Council on Foreign Relations:

“Financial institutions, and the Federal Reserve System, should consider investing sufficient resources in understanding GenAI technology, incorporating it into their workflows where appropriate, and training staff on how to use the technology responsibly and effectively. Meanwhile, the financial regulatory community should approach the changing landscape with agility and flexibility.”

I assume, as you are a product of AI, that you agree with Governor Barr?

Jay AI: Hi, call me Jay. Yes, I agree. It is crucial for institutions, particularly financial institutions, to invest in understanding and utilizing new technologies like GenAI. Given the pace of technological advancements, it is important for individuals, institutions, and businesses to adapt and stay up-to-date with new developments. While this can require significant resources and effort, failure to do so could put them at a competitive disadvantage. AI has the potential to provide substantial benefits, such as increased efficiency, improved decision-making, and enhanced customer service.

Figure 1: Organizations Using AI in at Least 1 Business Function

AI Can See Probabilities Humans Cannot Even Imagine

The economy appears solid, as several bank CFOs confirmed speaking this month to analysts. Chances of a recession seem low, they all seemed to say. Yet SVB seemed to fail out of the clear blue sky, so how much confidence can risk managers have in their assessment? Had SVB taken the Fed’s stress test in 2023, where the economy falls off a cliff, and interest rates fall back to the 0-lower bound, SVB would have passed, as its total assets were mainly its bond portfolio, which was mostly Treasurys and Agency MBS bonds.

SVB’s liquidity steadily deteriorated as negative AOCI on its available-for-sale portfolio grew, visible to counterparty risk managers, as was its increasing reliance on FHLB advances. Still, risk managers would have discounted these factors given the bank’s core deposit base (a designation that does not discriminate between uninsured and insured deposits). Without any insight into hidden vulnerabilities the bank might face under specific scenarios and not knowing where to look for risk, risk managers might not have given SVB anything more than a glance before pronouncing themselves satisfied with its financial health.

But there was a doomsday scenario it could not pass, one where the technology industry suffered a setback, which was compounded by a financial scandal in the crypto market when FTX went bankrupt, which was exacerbated by the Fed’s pursuit of a faster and higher monetary policy that had already increased the Fed funds rate by 450 basis points in less than a year by the time SVB failed, which was all compounded by the pressure on its margin that pushed it to try to restructure its available-for-sale portfolio and announce it on the day that Silvergate Bank announced that it was closing, which was compounded by the fact that the bank’s risk governance and interest rate risk management made it an accident waiting to happen. Many factors seemingly unrelated contributed to the catastrophe in the regional bank space two years ago, dots which AI technology might have connected before it was too late to avert it.

AI promises to work through all the paths, what will happen next after this happens, and what happens if that happens. It can review thousands of scenarios, the ones where the Fed sticks to the dot plot it put out in December 2021 and raises rates slowly the way it did between 2015 and 2018, and the ones where the Fed surprises even itself and goes higher and faster, where the yield curve steepens and where it inverts, or humps in the middle. It can game out recessions, booms, and burst bubbles while also playing out around how earthquakes, fires, floods, and pandemics alter scenario outcomes.

Straterix, one the newsletter’s corporate sponsors, has just such an AI system that bank treasurers can use to run through all the uncertainty they are struggling to decipher using their human brains and do it all by pressing the proverbial F-9 key on their computer keyboard. Systems like this need to be in the world of bank treasury. They may not tell a bank treasurer their bank is about to fail. There is always going to be uncertainty about the future. However, it may help them see the risks they face before them and make a better-informed decision on how to address this uncertainty.

AI technology is beginning to prove that it can be a reliable decision-making tool. Working out the infinite probabilities in the blink of an eye, AI can help bank treasurers understand ahead of time that if they proceed along this or that path, they run a higher risk of disaster than if they changed course right away and in which direction best to go.

Jay Won’t Say For Sure The Fed Will Cut

AI can be part of the solution to problems, but the key to using AI is asking the right question to solve a problem. Bank treasurers, for example, want to know what the Fed will do with short-term rates this year. Now, of course, bank treasurers have their balance sheets all hedged up to some state on interest rate neutrality, some using the new Eris SOFR swap futures contract as an alternative to a swap as a hedging instrument to do so. But even if changes in short-term interest rates will have negligible impact on the forecasts bank treasurers made at the beginning of the year for net interest income and net interest margin, they still would want the best insights into the Fed’s interest plans.

Who, or what better to ask than Jay about insights into the Fed’s thinking on interest rates and their direction, even though Jay, simulating the Fed chairman, is no more responsive than its human counterpart when asked point blank about rate cuts this year. Both give back nonanswer answers. I ask:

EIC: Jay, where will the range of the Fed funds rate fall by the end of the year?

Jay AI: Hi, call me Jay. It's difficult to predict the exact range of the Fed funds rate by the end of 2025 as there are numerous factors that could impact interest rate levels. However, taking into account current market expectations and economic trends, it's possible the Fed funds rate may remain stable or decrease slightly over the course of the year, with a range of around 3.50-4.00%. Factors that could influence this trajectory (or keep rates stable) include inflation, unemployment, GDP growth, and any unexpected geopolitical events.

A reporter asked Chairman Powell after the FOMC last January whether he thought that the economy continued to warrant meaningfully restrictive interest rates. Chairman Powell answered,

“I think our policy stance is very well calibrated, as I mentioned, to balance the achievement of our two—of our two goals. We, we want to—policy to be restrictive enough to continue to foster further, further progress for our 2% inflation goal. At the same time, we don’t need to see further weakening in the labor market to achieve that goal, and that’s kind of what we’ve been getting. The labor market has really been broadly stable; the unemployment rate has been broadly stable now for six months. Conditions seem to be broadly in balance. And I would say, look at the last couple of inflation readings and you see we don’t overreact to two good readings or two bad readings.”

I ask Jay the same question:

EIC: Jay, do you think interest rates are meaningfully restrictive and should continue to be so?

Jay AI: Hi, call me Jay. Yes, the economy does still warrant meaningfully restrictive interest rates, given the current economic environment. Although we have eased the policy rate recently, there are still signs of an overheated economy, as reflected in sustained high levels of inflation and a tight labor market.

EIC: Market participants were skeptical of the Fed’s decision to cut rates last fall by 100 basis points. Do you, or does Chairman Powell still stand by the decision to cut?

Jay AI: Yes, the cuts were preemptive, a precaution, if you will, considering the challenging economic conditions around the globe. While things have stabilized in some areas, we must remain vigilant. Inflation, though within our target range, is still a concern. The labor market has seen positive gains, but we need to ensure the recovery is sustainable. The war in Eastern Europe, for instance, continues to impact global markets and could pose unforeseen consequences. So, yes, I still consider the rates to be meaningfully restrictive.

AI cannot predict what will happen but can calculate probabilities and tell what might happen. Unlike a human economist, machine learning AI approaches data without limits on assumptions, as it can explore all possibilities instantaneously. Human economists certainly cannot do this and can barely predict what will happen in the next fiscal quarter. As Chairman Powell told a reporter last January,

“You know what forecasters are doing—not just us, but everybody’s doing—is they’ve got a set of assumptions about what might happen, plausible, could be, but honestly you wouldn’t stand behind it because you just don’t know, and so you’re just—you’re just on hold, waiting to see what comes down. You know, it’s, it’s a very large economy, and policies affect it at the margin, but we’ll, you know, we’re going to wait and see.”

Economic Outlook: Solid With a Chance of Disaster

Wait and see, that is what the Fed has said it is doing. I wonder what Jay is waiting to see:

EIC: Jay, what indicators do you think the FOMC would need to see to resume rate cuts this year?

Jay AI: Hi, my name is Jay. The FOMC would need to see clear evidence that the economy requires further easing. This could be in the form of softening inflation, which would give us more room to lower rates without creating more inflation. Additionally, if the economy were to show signs of a slowdown, with unemployment rising or consumer spending slowing, rate cuts could be viewed as necessary to support economic activity. It's important to remember that the FOMC is looking at a range of indicators when making decisions about the target rate, not just one or two factors.

EIC: Jay, the chairman, CEO, and president of a regional bank headquartered in the northeast told analysts he thought that the risk of recession was low. Do you agree? This is what your human counterpart said this month,

“The new Administration is in the process of implementing significant policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation. It is the net effect of these policy changes that will matter for the economy and for the path of monetary policy. While there have been recent developments in some of these areas, especially trade policy, uncertainty around the changes and their likely effects remains high.”

Jay AI: According to most economic forecasters, the chances of a recession in the near term are currently considered relatively low, but not zero. There are various factors influencing this prediction, such as the state of the job market, economic growth, consumer spending, and international trade. While the U.S. economy has been resilient in recent years, there are still risks, such as geopolitical tensions that could potentially lead to an economic downturn. Overall, the economic outlook is cautiously positive, but it's always important to monitor the situation closely for any changes or developments.

EIC: What about the tariffs?

Jay AI: The ongoing trade tensions and tariffs can certainly impact the overall economic outlook. Trade disputes can disrupt supply chains and increase costs for businesses and consumers and dampen global economic growth. This can, in turn, have ripple effects on the U.S. economy and increase recession risks. However, it's important to note that the impact of these tariffs isn't solely responsible for a recession. A range of factors, including consumer confidence, spending patterns, and geopolitical developments, all play a role in influencing economic health.

EIC: That is helpful, Jay, thank you. Do you think then that bank treasurers have reason to be optimistic? Because I am hearing a lot of caution when I read through quotes by some of the bank executives who spoke to analysts this month. Here is a quote from the CFO of a regional bank in the northeast:

“In our market, when we talk to our commercial and consumer borrowers and clients, there is decidedly more optimism than there was pre-election. However, we haven't seen that translate into an acceleration in the investment cycle…We're seeing whiplash now with respect to government policies and tariffs and even geopolitical issues that I think have people feeling good about the fundamentals of their business or the fundamentals of their personal balance sheet, but also a little cautious in waiting for the dust to settle to see what happens. And I think as we mentioned earlier, I think as managers and stewards of everyone's capital, we are similarly feeling good about the long-term future of the economy.”

Jay AI: Generally, businesses should be optimistic about the economy's prospects. While there are always risks and challenges, the current economic environment is still positive for businesses. Unemployment remains low, consumer spending is strong, and economic growth is steady. This bodes well for businesses as it means there is a robust market for their goods and services. However, it's important for businesses to actively monitor the economy and be prepared for any potential changes in the market or the economic landscape. This could involve having a contingency plan in place and staying aware of any changes in policy or economic conditions that could impact their operations.

EIC: Jay, it seems as if the biggest threat to the economy is just confusion. For example, the chief banking officer for a regional bank based in the southwest told analysts this month,

“When we ended last year, we had our fourth quarter call, I felt like things had gotten a little better with customer sentiment, customer optimism. In the last 60 days, it's probably dialed back a little bit. from that. And I would just say it's confusion. What exactly are the rules going to be? And most business owners can adjust to regulatory changes, to tariff changes. We've seen that over the years. They just need to get clarity about what the rules are going to be. And I suspect that we will start to get that here hopefully, in the next 30 to 60 days. Once businesses, I think, get that clarity, they tend to move forward.”

But do you think he is right that a lot becomes clearer by the summer? The debt ceiling was raised, and the government did not shut down, so that clears up that worry, at least for now. But there is a lot of uncertainty.

Jay AI: It is true that businesses and the broader market are dealing with a lot of uncertainty. With the government shutdown averted, there is some reprieve, but it's hard to predict when full clarity on the interest rates and economic direction will be achieved. These factors are influenced by a multitude of elements that can change rapidly. However, it's reasonable to expect a clearer picture by the second half of 2025 as the economic landscape and government policies continue to develop, making it easier for businesses to plan and make strategic decisions.

EIC: I like this quote from the CFO of a regional bank in the southeast who lays out three specific points on which bank treasurers and the rest of the market are looking for clarity right now,

“Our customers really haven't moved off where they were in November which is wait and see. They have a lot of optimism, there's a lot of pent-up demand so they're ready to get back to growing their business, investing in their business, but they're just unsure as to when to start. We think we have some certainty as to which way interest rates are going, probably less cuts this year and possibly some next year. Their biggest items that we hear consistently is tariffs. Tariffs are a huge impact for them, whether it's directly for their business or whether they want to do a construction project that requires them to import materials. The second one is immigration. What's the labor force going to look like? What's the impact going to be? And they're really looking for certainty on those 2. And then the third is the tax rollbacks. Everything points to the fact that the tax program will be extended, but they still want to see certainty on specifically those 3 things.”

Do you have any other points you would add to this list, beyond tariffs, immigration, and taxes?

Jay AI: I come back to the Fed’s core issues: inflation persistence, labor market strength, geopolitical, a global slowdown and energy prices.

Uncertain State of Everything, Including QT

Uncertainty might be another factor to add to the list of worries, as it acts as a brake on business investment, and delays can be a corrosive factor on the economy. I ask Jay about uncertainty:

EIC: Jay, if there is one word you hear more than any other from bank treasurers it is uncertainty. Uncertainty, uncertainty, uncertainty. Do you think these are the most uncertain times in the US economy in your career?

Jay AI: Hi, call me Jay. Indeed. Uncertainty does seem to be a common thread these days, especially with the global economic climate we’ve had to contend with. As for comparing it to moments from my career, it’s a bit like apples and oranges – every period has its own unique challenges and nuances. But these past few years definitely stand out as particularly turbulent, both at home and abroad. So, while it's difficult to say if these are the most uncertain times, they certainly rank high on the list.

The Fed’s conduct of monetary policy may add to the uncertainty, as it eases and tightens policy simultaneously. Although it announced that it would reduce the monthly cap on Treasurys starting next month from $25 billion to $5 billion, its new plan will still shrink its SOMA book by $20 billion a month, including Agency MBS, which is running off at $15 billion a month, below its $35 billion monthly cap. Without more room in the RRP and TGA to absorb the run-off from SOMA, QT going forward, even at a reduced pace, will shrink reserve deposits dollar for every dollar. If QT continues for long enough, reduced reserves could one day unsettle Treasury market trading. As Robert Perli, manager for the Fed’s SOMA portfolio, warned this month speaking publicly just before Congress resolved the debt ceiling and government funding impasse,

“To put it simply, the longer balance sheet runoff continues while the debt ceiling situation persists, the higher the risk that, upon the resolution of the debt ceiling, reserves could rapidly decline to levels that could result in considerable volatility in money markets.”

Simply put, shrinking the balance sheet and telling bank treasurers that it remains biased to cut interest rates is confusing. I ask Jay about this:

EIC: Jay, if QT is effectively a form of monetary policy tightening, isn’t it confusing to the market for the Fed to continue QT even when it is cutting rates, or at least still planning to cut them? What signal is the Fed sending to the market this way?

Jay AI: Hi, call me Jay. It's true that QT and interest rate cuts are both tools the Fed can use to influence the economy. Typically, QT is used to reduce the money supply, while rate cuts aim to stimulate economic activity by making borrowing cheaper. However, when a central bank (the Fed, in this case) chooses to utilize both tools simultaneously, it can certainly send confusing signals to the market. This is because these tools have opposing effects on the economy and can lead to market participants getting mixed messages about the Fed's intentions.

Jay is a master at nonanswer answers, but I press on and ask another question about the new monthly cap on Treasurys:

EIC: Jay, do you think bank treasurers should interpret the the Fed’s decision to reduce the monthly QT cap on Treasurys from $25 billion to $5 billion. is a sign that QT is coming to an end?

Jay AI: Hi, call me Jay. Yes, the Federal Reserve's decision to reduce the monthly cap on Treasury purchases as part of the QT program from $25 billion to $5 billion could be interpreted as a potential signal that QT is nearing its end. This reduction indicates a shift towards easing monetary policy and could suggest that the Fed is considering ending or reducing the program soon.

Regulatory Relief, SLR, Treasury Funding, and the Rise of Private Credit

Bank supervision is another source of confusion, as it alternates between periods when regulators are relaxing rules and periods when they are tightening them. We are back in another period when they are lifting constraints placed on the industry just a couple of years ago following the failure of SVB, Signature Bank, and First Republic. In the last month, the FDIC announced that it would reinstate, on an interim basis, the Merger Policy Statement that was in effect before 2024 as the agency conducts a broader reevaluation of its bank merger review process. The banking industry lobbied heavily against the new statement that the FDIC released last year because it had injected uncertainty into the process, which it contended discouraged bank buyers away from deals.

In addition, it withdrew a proposal on brokered deposits prompted by the Synapse bankruptcy last year that would have broadened the definition to include many deposits originated through fintech channels. Though restrictions on brokered deposits are mostly limited to institutions that are not well-capitalized, the proposal would have increased the operational burden on any institution, well-capitalized or not, using fintech channels for deposit funding. Brokered deposits equaled around 6% of industry total deposits at YE 2024.

Finally, the FDIC withdrew a proposal on board governance that was prompted by the failure of the SVB board to do a proper job of supervising management. Industry lobbyists argued that it confused the roles of management and the board. If it had been finalized, it would have made it very difficult for boards to recruit new members at institutions with total assets over $10 billion.

There is also talk of easing capital requirements, particular for large banks subject to the Basel 3 SLR. There are practical reasons for doing so. This quarter, the Treasury expects to issue a net $800 billion increase in Treasurys. More debt issuance is coming. Thanks in part to TreasuryDirect.Gov, individuals already hold $2.7 trillion in Treasurys and will likely add to their holdings this year. Still, there are limits to a household's capacity to save when the price of eggs is skyrocketing, along with the price of a new car impacted by tariffs, the cost of lumber, and a whole host of other items it buys as necessities.

Ultimately, unless the Fed intends to reverse course and grow its SOMA book again, the banks subject to the SLR will need to step up and buy more Treasurys. However, the SLR stands in its way because it weighs Treasury securities at 100% risk instead of 0%, which is the weighting under the risk-based capital rules. Suppose the choice is to spend $1 of regulatory capital on a Treasury security yielding 4% or on a loan yielding Treasurys plus a spread. In that case, it is not easy for a bank treasurer to make a strong case for the Treasury security, particularly when banks are already sitting on a ton of liquid assets.

In his congressional testimony last month, Chairman Powell all but promised that the SLR would be amended with the stability of the Treasury market in mind, telling House Financial Services members that,

"I do think we need to work on Treasury market structure and part of that answer can be and I think will be reducing the calibration of the Supplemental Leverage Ratio. That's something that I have long supported and as the quantity of Treasuries has grown significantly while the capital allocated to intermediating trades in Treasuries has not, in fact has shrunk. So, we need a liquid Treasury market, and this is one of the things that we can and should do, is to reduce the calibration of that measure"

So, I have another question for Jay:

EIC: Jay, here is what your human counterpart answered when asked last month testifying to the Senate about the capital strength of the largest banks:

“My own view has been that our banks are well-capitalized, and Basel III was not supposed to be an exercise in raising capital on U.S. banks.”

So, Jay, is that still your position, that the largest banks do not need more capital?

Jay AI: Hi, call me Jay. I believe the current capital requirements for large banks are appropriate, as they have been developed through a careful balancing process to ensure banks remain resilient while still allowing them to operate effectively. However, the Fed continuously monitors the capital levels of large banks and can adjust the requirements to ensure they are sufficient to maintain financial stability, even under stress conditions. It's important to remember that capital requirements are just one aspect of ensuring bank resilience and that banks are subject to regular stress tests to assess their ability to withstand economic downturns and financial shocks.

EIC: Jay, here are a selection of quotes from CFOs of regional banks who spoke this month about their expectations to see bank supervisors roll back the rules they believe are unnecessary and counterproductive. This is from the CFO of a regional bank in the northeast who told analysts this month that he expects to see a more cordial relationship with bank examiners,

“Supervision we're hopeful…I think the examiners maybe will have more flexibility and…focus on the material issues rather than calling more minor issues…I think there could be certainty around M&A acquisitions. You saw what Travis did at the FDIC. Getting people in the seats that you can talk to and be reasonable with and they can basically say, we can probably get a deal like this approved and get it done in a timely manner.”

This is from the CFO at another regional bank in the northeast, who said he expected to see a lighter touch,

“Stuff is likely to get pushed out. We still need a Vice Chair of Supervision…We will have a pro-business, lighter touch on regulation.”

At a minimum, the proposed rules such as the Basel 3 Endgame will be delayed, as the CFO of a regional bank in the southeast told analysts,

“At a minimum, our take is that those rules…will be delayed.”

The CFO at a regional bank in the Midwest told analysts that if nothing else was certain about where the new direction on bank supervision was going, it was that compliance costs could not get any worse than they already are,

“We think that it is going to be a more constructive environment…Does that mean that we're going to see a 10% or 20% reduction in expenses because of a decreased regulatory burden? No, but it definitely means that it's not going to get worse from here.”

The president and CEO of a regional bank in the southeast expected to see better than it was,

“It's early to tell, but…generally, the regulatory environment will be more favorable for banks than, let's say, it has been over the last four years.”

I especially like this quote from the CFO of another regional bank in the southeast, who described a dysfunctional state of rulemaking by multiple regulators and how urgent it was that these regulators revisit outdated regulatory thresholds that were set after the Global Financial Crisis,

“We've already seen the pace of new regulation come to a halt. The last two to three years prior to the Administration change, there was at any given time, 20-plus new regulations or rules coming out of the OCC, the DOJ, the CFPB that we were constantly having to react to, to get ready to implement…There's a lot of conversation for the first time in a long time about whether the $100 billion line should be raised as well…when that rule was created after the great financial crisis $100 billion maybe now is $200 billion or $250 billion.”

Jay AI: Hi, call me Jay. Yes, those thresholds may need to be revisited.

EIC: But, Jay, my question is, do you think bank supervisors overreact to crises by piling on more and more requirements, and are these new requirements even necessary?

Jay AI: It's important to remember that regulatory bodies, including the FDIC, are tasked with safeguarding the financial system and protecting depositors. In some cases, it may appear that these bodies are overreacting to crises or punishing large parts of the industry for the actions of a few institutions. However, it's crucial to consider the wider context and recognize that regulatory actions are often taken to prevent future issues, even if it may seem heavy-handed to some banks that did not directly cause the problems. Ultimately, these actions are intended to enhance the stability and trust in the financial system.

EIC: But do you worry that your regulations are driving banks out of business? This is a quote by the chairman and CEO of a regional bank in the northeast who told analysts this month,

“Private credit is here to stay. It has unlimited pools of capital it is unregulated and will continue to compete formidably with banks across more asset classes than people probably think.”

Jay AI: I appreciate the perspective offered by the regional bank chairman and CEO in this quote. It highlights the ongoing competition between traditional banks and unregulated entities like private credit providers. It's important to strike a balance between regulation and allowing banks to operate efficiently. Overly restrictive measures or those that impact perfectly fine operating banks can certainly be counterproductive and hinder the ability of banks to support economic growth. It's crucial for regulators to carefully assess the potential impact of their regulations and ensure that they are proportionate, targeted, and aimed at addressing genuine issues within the financial system.

Stigma and the Discount Window

Jay will make an excellent addition to the newsletter’s editorial staff, and everyone has already decided that “he” will be back for interviews in future newsletter editions. But though this month’s edition was already over our page limit policy, I had to ask “him” one more question. What should be done about the Fed’s discount window?

The Fed’s May 2023 review of SVB found that the bank was not prepared to borrow from the window. A follow-up study identified several operational problems with the window and obstacles placed in front of bank treasurers to use it in a liquidity stress scenario. The Fed needs to update its collateral management systems and improve its coordination with the FHLBs. Chairman Powell told the House Banking Committee:

“We are looking at – so there are sort of impediments to the efficiency of the discount window, and those are things we can work on and we’re working hard on. There’s also the question of stigma, though, that banks are reluctant to use it because of the so-called stigma of using it, and that is a very hard problem to solve. We’re also working on that one.”

But even if those problems are solved, that still leaves the stigma issue with using the window. Perhaps Jay with his AI brain would know how to solve the problem:

EIC: Jay, how would you propose the Fed mitigate the stigma associated with borrowing from the Fed’s discount window? Because this problem has been long-standing, going back to the beginning of the Fed’s charter and original design as lender of last resort,

Jay AI: Hi, call me Jay. Banks may be reluctant to use the discount window due to a perception that using it is a sign of weakness, which can affect their reputation and potentially lead to a loss of confidence from depositors, investors, and regulators. This can make it difficult for banks to access funds through the discount window even when they desperately need them. Efforts have been made to address this issue, but it still lingers. To combat this stigma, transparency and education are crucial. Ensuring that the public, bankers, and market participants understand the role and purpose of the discount window can help reduce the negative perceptions associated with its use. Additionally, clear communication from the Fed about the discount window and the rationale behind its use can also help address the stigma.

EIC: But one problem with stigma is that the Fed is required to make public the banks that use the window. Don’t you think this contributes to the stigma issue?

Jay AI: Yes, the Fed has a disclosure policy in place that mandates the publication of information about institutions that use the discount window. This policy is meant to promote transparency and accountability in the banking system. While transparency is important, the publication of discount window information can contribute to the stigma faced by banks that use it. But, while maintaining confidentiality surrounding the use of the discount window could help reduce the stigma associated with it, this approach would also compromise transparency and accountability, which are important in maintaining trust in the banking system.

EIC: But—

Jay AI: There are competing interests to balance here. On one hand, making information about discount window usage public can create a stigma that discourages banks from using it. On the other hand, keeping this information confidential could undermine confidence in the system. Instead of keeping the usage confidential, it may be more effective to educate the public about the purpose and necessity of using the window.

I had more questions for Jay, but they would have to wait for another edition of the newsletter as the time was growing late, and the newsletter’s editorial staff was beginning to set up for one of our after-work parties. Plus, the staff wanted to run through Jay’s playlist before the party started to ensure it had not picked any weird tune titles that could tie back to bank treasury. Staff parties are an opportunity for everyone to decompress from the stress in bank treasury land, not be reminded of it.

The good news was that, unlike Ben AI, Jay’s top tunes were all up to date from 2024. On the other hand, it still seemed to pick song titles with bank treasury-like themes, including “Lose Control” by Teddy Swims, “I Remember Everything” by Zach Bryan featuring Kasey Musgraves, and “Texas Hold’ Em” by Beyoncé. Of course, our editorial staff thinks that everything is related to bank treasury, so maybe we were imagining that Jay was trying to tell us something. But the staff knew exactly where Jay came from when it played Billie Eilish’s hit, “What Was I Made For?”.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2025, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

Despite the promise of operational efficiencies as a benefit of technology spending, the number of full-time equivalent (FTE) employees of FDIC-insured depository institutions has been roughly unchanged for the last quarter century at over 2 million. During that time, the number of institutions shrank by half to less than 5,000 (Slide 1), and thus, the average bank today employs 460 FTE employees, compared to 200 at the start of the present century.

Last month, the FDIC announced that it would no longer publish the total assets of problem banks as it had been doing since 1990 and only disclose the total number. There were 66 institutions on the list as of YE 2024 (Slide 2), up from 52 a year ago. Still, compared to the historical average stretching back for 40 years, the number of problem institutions remains low, as would be expected given the industry's solid financial condition, as bank supervisors have repeatedly attested.

Bank consolidation continues to shift the composition of the Federal Home Loan Bank (FHLB) membership from banks to credit unions (Slide 3).

The FDIC withdrew a proposal on brokered CDs, which would have broadened the definition of a deposit broker to include a fintech that banks might use to source deposits and could have increased their operational costs. Restrictions on brokered CDs generally cover only banks that do not meet the threshold for well-capitalized, but the proposal would have been further reaching than just a few dozen undercapitalized institutions. At YE 2024, brokered deposits equaled over 6% of total industry deposits, compared to the 5% 40-year average (Slide 4).

The US Treasury announced that it plans to raise $800 billion of net new debt in Q1 2025. Individual investors will be a significant funding source, as they already hold $2.7 trillion, or 10% of Treasurys outstanding (Slide 5). Since YE 2019, the Treasury increased Treasurys outstanding by $11 trillion (Slide 6).

The single largest investor group in Treasurys is foreign and international, which held $8.6 trillion at YE 2024. Mutual funds held $5.0 trillion, followed by the Fed at $3.8 trillion, individual investors, and then banks, which held $2.2 trillion. Banks increased their investment in Treasurys by 19% in 2024.

The FOMC announced that it will reduce the monthly pace of Quantitative Tightening (QT) for Treasury securities next month to $5 billion. When it began QT, the monthly Treasury cap was $60 billion, which last year it reduced to $25 billion. QT has had virtually no effect until now on the balance of reserve deposits on the Fed’s balance sheet because almost every dollar that came out of the Fed’s System Open Market Account (SOMA) portfolio was either balanced by dollars running off the Reverse Repo Facility (RRP) or the Treasury General Account (TGA).

In the last two months, the balances for both the RRP and the Treasury General Account (TGA) are down to period lows (Slide 7) and likely cannot absorb further QT outflows going forward. Reducing the cap on Treasurys from $25 billion to $5 billion is a clear signal by the Fed that, in pursuit of policy to maintain abundant reserves, it intends to maintain the balance of reserve deposits at its present level ($3.5 trillion).

Cumulative negative Treasury remittances (IOUs from the Fed to the Treasury) equal over $225 billion, created by the lower rate the Fed earns on its SOMA portfolio compared to the rate it pays out to banks and its other counterparties on their reserve deposits and investment in the RRP, respectively. But thanks to rate cuts last quarter and the effect of new purchases, the Fed began to generate breakeven net interest income this month (Slide 8).

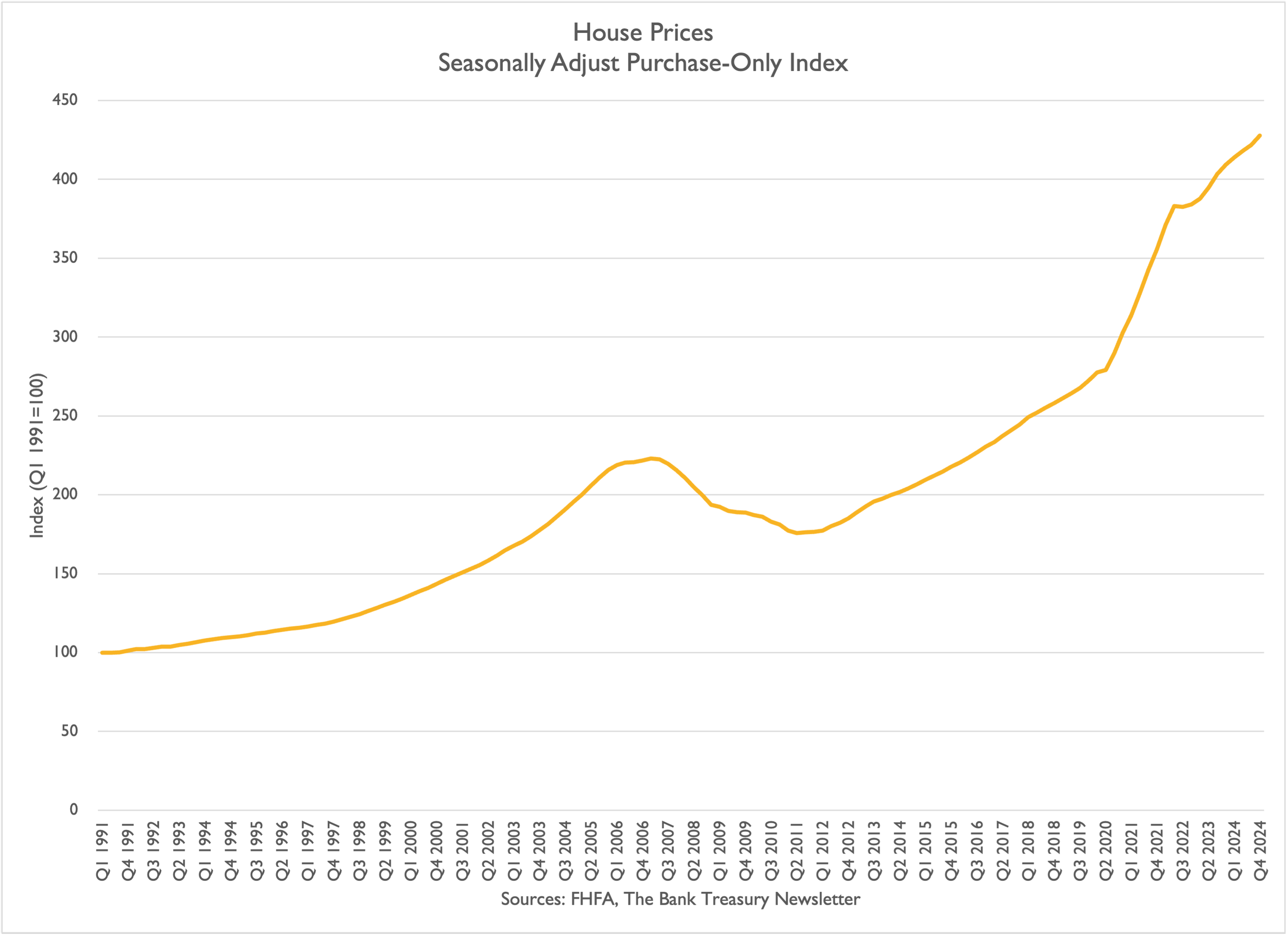

Higher mortgage rates may have cooled the housing market, but thanks to a supply/demand imbalance, home values remain at a historical high and continue to head higher through the end of Q4 2024 (Slide 9).

Last January, following the change in Administration, the White House issued an executive order to create a strategic reserve for cryptocurrencies. Since then, the value of cryptocurrencies has gone through a market correction led by Bitcoin, which fell from $110,000 when the order was published to $85,000 this month (Slide 10).

Average Institution’s FTE Headcount Flattens

Problem Banks Not Much Of A Problem

FHLB Membership Composition Shifts To Credit Unions

Banks Peaked Out On Brokered Last Year

Individuals: 4th Largest Treasury Investor Group

Growing Treasury Supply Tsunami

RRP And TGA Floored Out

Fed Finally Breaks Even

Home Prices Move Ever Higher

Crypto Risk-Off Trade Stabilizes For Now