BANK TREASURERS AT 20

The IMF increased its projection for U.S. GDP in 2024 from the 2.6% it projected last July to 2.8% and improved its projection for 2025 from 1.9% to 2.2%. Behind these projections, the IMF assumes that as U.S. fiscal policy gradually tightens and the labor market cools off, consumption and the economy will slow, too. Yet, to date, the U.S. economy has been resilient, as the U.S. Bureau of Economic Analysis's third estimate for Q2 2024 GDP went up to 3.0%, from 1.6% for Q1 2024, driven by consumer spending. Inflation has slowly fallen in line with the Fed's long-term target of 2%.

Consequently, bank treasurers, who had already been skeptical about the forward curve's implied pace of rate cuts for this year and next, even before the 50-basis point cut last month, have grown even more skeptical about the logic and the wisdom of further rate cuts this year. The CME Fed Monitor, which only a few weeks ago had calculated the odds of a 50-basis point cut on November 7th at more than 50%, pegged the current probability for 50 basis points on November 7th at 0% and raised the likelihood of a 25-basis point cut to over 90%. Rate cut projection volatility is but part of the main story in the market today, which is its continued volatility with rates in the intermediate and long end of the yield curve back over 4% and mortgage rates back to their highest level since the summer. The CBOE Volatility Index is the highest it has been in a year.

There are two groups of banks today. Those with bond portfolios that are deeply underwater, are dealing with negative Accumulated Other Comprehensive Income (AOCI), and are technically insolvent, and those who had the wisdom or luck to hold back from buying bonds in 2020 and 2021 and stayed in cash. Group A is stuck in a difficult situation but has no choice but to wait for its underwater holdings to mature at par value. Group B struggles with whether to commit to cash or shift into bonds tied to the intermediate part of the yield curve. As their cash balance contributes to their asset sensitivity, many bank treasurers must find solutions to protect their balance sheet as the Fed's rate-cutting cycle continues. Notably, the fundamentals support bond investment at current rates as the bond term premium is positive.

On September 30th and October 1st, the Secured Overnight Financing Rate (SOFR) spiked up by 21 basis points, from 4.84% to 5.05%, before falling and settling back to 4.83, over the 4.80% rate the Fed currently pays for funds parked in its overnight Reverse Repo facility (RRP). The spike in SOFR over the month's end was the first spike in the rate since September 15 and 16, 2019, when SOFR jumped by 305 basis points to 5.25%.

The SOFR spike in 2019 was caused by insufficient reserves in the system, which banks hold to manage their liquidity and make payments over FedWire. Bond settlements and tax payments combined led to a sudden shortage of reserves and caused a liquidity crisis in the repo market. The Fed had also just completed Quantitative Tightening (QT) that summer, reducing the balance of reserves from $2.5 trillion to $1.5 trillion. Bank treasurers now wonder whether the spike in SOFR over month-end means the same thing, that the Fed may be going too far on Quantitative Tightening (QT) and that balance sheet normalization is ending. However, the difference between QT1 and QT2 is that since QT2 began in Q3 2022, the balance of reserves has remained over 3 trillion, more than twice the level of reserves that existed in September 2019.

Bank treasurers remain hopeful that the yield curve will normalize over the next year, which they believe will help them widen their net interest margins (NIM) and drive their net interest income (NII), both of which have been under pressure. Analysts have focused on the path for deposit repricing betas as the Fed cuts interest rates. Notably, the industry's cost of funding, including noninterest and interest-bearing deposits, equaled 3%, the highest funding cost since the eve of the Global Financial Crisis (GFC). However, the spread between the cost of funding and the effective Fed funds rate has never been wider, going back to the turn of the century. Thus, bank balance sheets are well positioned to improve NIM and NII next year, assuming low-yielding assets continue to run off and are replaced with higher-yielding earning assets.

Office commercial real estate remains a flashpoint for banks, as the outlook appears to worsen. Yet a key message on analyst calls this month is that asset quality remains well-reserved and that Current Expected Credit Loss (CECL) reserves are sufficient to cover the risk. Some bank managers even suggested on their analyst calls this month that credit reserves might come down next year.

The Bank Treasury Newsletter October 2024

Dear Bank Treasury Subscribers,

The hardest thing about writing a monthly newsletter for the past 20 years this month is not coming up with newsworthy items to report. Maybe it might seem that way to people not in the bank treasury world to think about the topic as so much paint drying on a wall that it is a wonder how we have not said everything that needs to be said on the subject after 20 years. But as bank treasurers know, their world is anything but dull, and trying to keep up to date with it is neverending.

And so much has happened in the space since we launched the newsletter in October 2004, even if it is all cyclical. In the past 20 years, the country has had four U.S. presidents, and by next month, we will know who will be the fifth. There have been 20 World Series, although none since 1981 between the Yankees and the Dodgers when your editor-in-chief was just beginning to talk to bank funding desks.

The Fed has been under the leadership of four successive Fed chairs who have led three rate-hiking cycles and, under Jay Powell, is now in the process of a third cutting cycle. His term ends in 2026. It is a cycle that the newsletter’s subscribers are still trying to process. They seem confused lately about why the Fed seems intent on cutting the Fed funds rate when the economy appears strong, and inflation is not yet fully contained.

You know you can learn a lot from talking to bank treasurers, as our staff writers always discover after a call with one of them. Thus, they tell us they are confused by what the Fed is doing, but this just means they are not satisfied with the explanation of why the Fed decided to start cutting now. Of course, they understand that there are appearances and realities regarding the Fed.

Thus, it “controls” interest rates, but only the overnight rate, as was made plain when the Fed’s 50 basis point cut last month led the long end of the yield curve to rise and take mortgage rates along with it. Its monetary policies may or may not have some impact on inflation, although the latest data makes that assertion somewhat debatable. Raising the Fed funds rate or lowering it just signals a direction that the Fed wants interest rates to go in. It takes a market to get anything real done across the yield curve.

Even the whole lender of last resort thing that the Fed keeps hammering on because banks do not borrow from it in emergencies is not much more than a slogan. The reality is different. No bank treasurer in their right mind would want to borrow anything from the discount window or even that daylight overdraft window it maintains. And many bank treasurers say that the folks at the window do not exactly make it that easy to borrow from the window. It is all theoretical.

If your counterparties knew that you were that desperate, they would pull all their lines with you immediately, and your large depositors would stampede. And even if it all stayed a secret (which it will not), the Fed is under no legal obligation to lend to a member bank, even one that met all the regulatory thresholds for safety and soundness. But like a safety net you never need, the Fed as lender of last resort serves a purpose, if only so bank managers sleep a little better at night.

Do We Really Have To Cut?

Bank treasurers say they are confused, but you learn over the years from talking to them that they know all the unsaid truths, that the only reason why the Fed is cutting is to hike rates again when it needs to, and visa versa. There is no actual signal with the 50 basis points that the voting members of the FOMC see trouble ahead.

But who would not be confused by a rate called r*? Maybe the neutral rate the Fed says it sees is just a mirage, and even if it is a real thing, it seems to move around a lot for something that is not directly observable. Basing monetary policy does not seem like a very reliable approach to setting interest rates.

Bank treasurers can also see the irony of describing the Fed’s rate changes as data-dependent. They still talk about the time in December 2015 when the Fed commenced a hiking cycle when both GDP and CPI were clocking in at under 1%, just as now the Fed has begun to cut rates, when real GDP for Q2 2024 was just revised up to 3% and September 2024 CPI came in at 2.4%. Data dependence, like the lender of last resort, is in theory. Reality is another matter.

There is never a dull moment in the bank treasury space, and there is much to discuss. Our subscribers talk a lot about the forward curve. The forward curve has been all over the place, like r*, paying you and not paying you to extend and go long or to hold on and stay short. The forwards are an evergreen topic in the world of bank treasury. As far as most bank treasurers are concerned, the only certainty in the forwards is that they will change, as the chairman and CEO of a GSIB told analysts this month,

“The one thing I can assure you is the forward curve will not be the same forward curve in six months.”

The same can be said about the net interest margin (NIM). We covered the story when it was widening and when it was narrowing. We detailed trends in the loan-to-deposit ratio, tracked loan demand’s ups and downs, and noted what bank treasurers have said about loan and deposit pricing betas. This is where bank treasurers read all about it, the nitty gritty stuff such as the term premium, when it was positive like it is now, and when it was negative for most of the last decade. We talked to bank treasurers eyeing bond duration extension trades in their investment portfolios and those looking for an excellent argument to make to the board of directors for holding off and staying in cash.

Sit in cash or extend now? The term premium on a 10-year 0-coupon bond increased in the last month to 35 basis points, up from 0, which means that an investor in a 0-coupon bond for 10 years would earn more than an investor in overnight risk-free assets and rolling that asset for the same time. But it may become even more rewarding. Last April, the term premium was over 50 basis points. Bank treasurers are divided. The CFO of a large regional bank headquartered in the northeast told analysts that his bank was shifting cash from the Fed into bonds,

“We are putting more money into the investment portfolio…we will continue to grow our investment portfolio…From a cash-at-the-Fed perspective, we…probably will go lower but not much lower.”

The CFO at a GSIB was on the other side of the trade, telling analysts,

“The choice to extend duration is about balancing the volatility of NII against protecting the company from extreme scenarios. And so right now, if we wanted to extend…we certainly could, we have the capacity inside the portfolio. But for now, we're comfortable with where we are.”

There are two-way markets with everything discussed in this space.

This is where bank treasurers go to read about the Fed’s monetary policy’s ebbs and flows, easings and tightenings, and balance sheet expansions and contractions, but also where they go to dive into the banking industry’s latest balance sheet trends and popular hedging and investment strategies. They want to learn how to use Eris SOFR swap futures contracts to execute a fair value hedge for their available-for-sale (AFS) securities portfolio or as a cash flow hedge.

But that’s not all. Because our subscribers’ business brief goes beyond devising a balance sheet strategy and gaming out the next move on rates by the Fed, they also need expertise in bank regulatory policy. That is another reason they come here.

The newsletter has been there. It pays to have a long memory because otherwise, it is tough for newly minted bank treasurers to appreciate how things today got the way they did. Our staff writers can go into as much detail as you would like and go through the long history of what they have written on bank regulations. Because they were there, and remember when regulators were busy relaxing rules for a decade leading up to the Global Financial Crisis (GFC) to make it easier, for example, for banks to include Trust Preferred securities (TruPs) in their capital calculations. Then, after the GFC, they reversed and banned TruPs in regulatory capital. Talk about consistency!

But our staff knows all about it. They know why regulators thought it would be a great idea after the GFC that the largest banks calculate their risk weights for their exposures under an advanced approach that was very complicated and not very transparent. They could go into all the gory details how calibration became a buzzword in regulatory circles, what rules regulators eased in 2018 in line with calibration, and what rules they now propose to recalibrate the other way. No regulatory detail is ignored, and it is no surprise to anyone here that the FDIC may disapprove a reproposal of the Basel 3 Endgame because its board is split. Our staff have been reading board member speeches for years.

And our subscribers want those details, as the CFO of one of the GSIBs told analysts who wanted to know what he thought of Vice-Chair of Bank Supervision Michael Barr’s announcement in a speech he made last month that regulators would pull the proposed Basel 3 Endgame and release a new proposal,

“We actually need to see the proposal because the details matter…focus is on hoping to see the proposal so that we can process the detail and continue advocating as appropriate.”

Monetary policies tighten and ease, margins narrow and then widen, deposit and loan balances vary with the season, and the Fed’s balance sheet expands and contracts. Regulations and regulators come and go, too. Dan Tarullo was the unofficially-designated Vice Chair of Bank Supervision a decade ago. He was busy during his four-year term, tightening bank regulations after the GFC. He was succeeded by Randy Quarles, who had the role officially and set off trying to calibrate the rules that his predecessor had tightened. Then came Michael Barr, and regulations are being retightened again.

That is the bank treasury business. After reporting on a few of these never-ending cycles, some may conclude that they have seen it all. Still, in the bank treasury space, there is always a surprise, an unexpected outcome, the price of uncertainty in unpriced short optionality inherent in bank balance sheets comprised of fixed and floating rate assets and liabilities with term and non-term maturities that pay off at par.

Another thing bank treasurers know for sure is that rate hikes can cause damage somewhere in the financial plumbing, upset the fabric of liquidity floating around in the bank treasury universe, and break someone’s profit and loss account. Small ripples can cause panic seemingly from nowhere. They have seen this many times. And they want to be prepared. They know that nothing happens, and then everything happens. Even though bank treasurers have seen it all before, they are still surprised when the inevitable snap snaps. Hence, they are a cautious bunch. As the chairman and CEO of one of the GSIBs reminded analysts, cash is king in volatile times like these,

“Cash is a very valuable asset sometimes in a turbulent world. And you see my friend Warren Buffett, stockpiling cash right now.”

The Newsletter’s First Rate-Hiking Cycle

Because even certainty has its drama, the unexpected outcome that comes out from nowhere. Thus, when the newsletter launched in October 2004, Fed Chair Alan Greenspan was already leading the FOMC to raise the target Fed funds rate by 425 basis points in 17 well-communicated quarter-point increments from July 2004 to July 2006, from 1% to 5.25%. At that time, just as market participants complained in March 2022, he faced a chorus of complaints leading up to the first hike in 2004 that the Maestro had kept rates too low for too long. He had taken the Fed funds rate down to 1% after 9/11 and the start of the wars in Afghanistan and Iraq, the last time the market was in the grip of a major panic, but now he was holding back too long from hiking them.

The hiking cycle that followed that first hike in July 2004 was unprecedented in its predictability. Breaking from past Fed conduct, Fed policy became an open book. Forward guidance, as it was called, was also the bane of every derivative trader who blamed it for killing their vol trading business, which thrives on directional uncertainty and volatility. Because it is tough to make money when everyone knows the Fed’s next move precisely, fixed income might be dull, but it has its moments.

But maybe too many moments, as today’s forward curve reflects a market view on the Fed’s next move on rates that has been all over the place. Thus, the CME’s FedWatch Monitor pegged the probability that the Fed would cut the target Fed funds rate by 50-basis points on November 7th at 53% on September 24th last month, which fell to 0% two weeks later, while the probability of a 25-basis point cut went from 50% to 93%. With so much market volatility, it is no wonder the CFO from one of the GSIBs told analysts the bank was reluctant to give earnings guidance too far out in advance,

“We'll provide guidance, I think, for 2025 when we get back together again a quarter from now. Part of the reason we try not to do it too far in advance is because an awful lot moves with the rate curve. Remember, this year, at one point, we had six cuts, another point, we had one cut. And even this past quarter, the market was surprised with an extra cut.”

Because the rate outlook is so volatile, decisions made a lot of sense a month ago do not seem as intelligent today. The head of commercial banking at a large regional bank in the northeast tried to explain why he terminated some of his received fixed rate swaps last quarter because he believed that rates were going to fall a lot faster than they seem likely to fall now, telling analysts,

“During the third quarter…the yield curve was counting as many as seven or eight cuts through the second quarter of next year…So, we opportunistically chose to terminate swaps during the third quarter given those expectations…We felt that was a good risk reward to lock in that benefit…and protection against lower rates.”

The hiking cycle, which Mr. Greenspan ultimately left to his successor, Ben Bernanke, to finish when the latter became Fed Chair in February 2006, caused the Treasury yield curve to flatten, took all the fun out of rolling down the curve, and all the juice from extension trades. However, that just gave rise to more innovative trades that bank treasurers considered when the risk-return tradeoffs offered in their conventional investment and funding strategies just couldn’t do it for their NIMs and interest income anymore.

There is always surprises lurking around the corner in the bank treasury space, even for the most seasons treasurers. Bank treasurers like to rank liquidity over profitability when listing the objective of their bond portfolios and always dismiss credit as something more appropriate in their loan books. But when the Fed squeezed yield out of spread product when it hiked rates between 2004 and 2006, they stopped immediately dismissing fixed-income product offerings in non-agency Residential Mortgage-Backed Securities (RMBS), Commercial Mortgage-Backed Securities (CMBS), and Collateralized Loan Obligations (CLO). Their refusals eased to skepticism, attracted to the yield pick-up these bonds offered over traditional Agency MBS and Treasurys. And then, when they blew up in the faces during the GFC, they were surprised.

SOFR Spikes

No, the hardest thing about writing this newsletter is not figuring out what to write about each month. It is deciding as your editor-in-chief what to leave out. It is being the editor on a subject so detailed that a newsletter coming out once a month leaves us space-constrained to recount everything on the minds of our readers. Some months, accounting will take center stage. In other months, it could be deposit pricing or loan beta. What our editorial staff decides to write about each month and what your editor-in-chief ultimately chooses to keep in this month’s edition or save for next month’s just depends.

On what? Well, on you, our readers, and what is fresh on your mind. Let’s face it: Who doesn’t suffer from a little attention deficit in this industry? Things pop up, as in the 21-basis point spike in the Secured Overnight Financing Rate (SOFR) over month-end (Figure 1), the first spike of this magnitude since the SOFR spike in September 2019, when it surged by 300 basis points, to 5.25%.

Was this a sign of trouble in the repo market? Was there a shortage of reserves deposits, as happened in September 2019? There was a surge in sponsored repo volume over month-end which which is detailed in this month’s edition of the chart deck. This could reflect pressures on primary dealer balance sheets. It's hard to say, but the balance of reserves has been stable at $3.2 trillion since the beginning of QT, more than twice the reserve balance in September 2019.

Another $40 billion of Treasury Notes, Bonds, and agency MBS rolled off its System Open Market Account portfolio over the last month, leaving it with a balance of $6.6 trillion, about $3.0 trillion more than it had in September 2019. But the CFO of one of the GSIBs was convinced that the SOFR spike over month-end meant that the Fed's QT days are ending.

“The argument is that the repo spike that we saw at the end of this quarter was an indication that maybe the market is approaching that lowest comfortable level of reserves, that's been heavily speculated about…that number is probably higher and driven by the evolution of firm’s liquidity requirements…When you put all that together, it would add some weight to the notion that maybe QT should be wound down. And that seems to be increasingly the consensus that's going to get announced at some point in the fourth quarter.”

Figure 1: SOFR

Topics du jour come and go. We paid a lot of attention to the LIBOR transition, its phase-out that ended in 2021, and its replacement with SOFR. So much electronic ink was spilled on the subject, and concerns from our subscribers over the inherent flaw in replacing a term credit-sensitive benchmark with an overnight, risk-free rate. Bank treasurers worried that a credit-sensitive rate might shoot up in a liquidity panic while a risk-free rate could go the other way and lead to a credit crunch. They worry about such a scenario today, and sudden SOFR spikes, as happened over month-end, only contribute to their problems sleeping at night. And it is not just the spike that worries them about the state of the money markets when they can also point to general collateral repo trading above SOFR and even over the top of the band on Fed funds.

Credit-sensitive benchmark rates are available as an alternative to SOFR. Credit add-ons for SOFR have been developed. But these efforts remain unblessed by regulators, and their take-up in loan documents has been limited. For all the worry that the transition would lead to problems in lending, the floating rate market’s transition from LIBOR to SOFR is done without much of a noticeable hitch. SOFR is not to blame for the industry’s soft loan business.

CECL and Loan Demand

Current Expected Credit Loss (CECL) was another hot topic in this space, which became GAAP in 2020, right before the Covid lockdowns. Talk about timing! The accounting rule was expected to cause problems for lenders, given that it required them to hold credit reserves for the life of the credit exposure on the day it was funded. Loans made at the height of a downturn in the credit cycle might require higher reserves than if reserves were calculated under the then-existing accounting standard that limited provisions for credit losses for those that were estimable and probable over the foreseeable future, typically two years.

A bank's CECL reserves could theoretically exceed 1.25% of risk-weighted assets. As bank treasurers know, credit reserves over 1.25% of risk-weighted assets are deducted from Tier 2 regulatory capital unless you work at a bank with total assets over $250 billion and can calculate your risk-weighted assets using an advanced approach. They feared in the lead-up to its implementation that, in a credit downturn, CECL combined with the calculation of regulatory capital could limit a regional bank's appetite to lend, as the added capital burden would reduce the exposure's return on equity.

Yet, Covid and the stimulus programs, not CECL and not SOFR, are to blame for negative loan growth in 2020 and 2021 outside of Paycheck Protection Program loans. They have had no apparent connection to the banking industry's current loan business and why it has been so soft lately, even as the economy remains a growth machine. Loan growth averaged just 1% year-over-year over the last six months.

The previous month's H.8 data for commercial and industrial loans showed that annual growth last month was 5% (Figure 2). But, you would need more than a month of data to tell whether the previous month's pick-up was a sign of something different, that loans are back to growth mode. The Fed's senior lending officer survey still paints a dismal picture of loan demand. More likely, last month's seemingly encouraging sign of some green shoots was just a one-off, perhaps spurred on by the Fed's 50-basis point cut, a surge of business reacting to a market opportunity that will fade in Q4.

It is hard to say. The CFO of a Global Systemic Important Bank (GSIB) was mainly of the opinion that last month's pop was opportunistic business getting done. But then again, maybe it was more than just a blip.

“Some of that Debt Capital Markets outperformance is opportunistic, deals that aren't in our pipeline and those are often driven by treasurers and CFOs seeing improvement in market levels and jumping, jumping on those. So, it's possible that that it's a little bit a consequence of the cuts. But I think I mentioned you know, we did see for example, a pickup in mortgage applications and a tiny bit of pickup and refi in our multifamily lending business, there might be some hints of more activity there.”

The chairman and CEO of the same GSIB believed the pop in business in capital markets last quarter was just opportunistic. Because there is one thing bank treasurers know, a good thing does not last forever. Sometimes, you hit that bid or lift that offer today because waiting until tomorrow may be too late; as he told analysts,

“In the debt markets, you know, rates came down, spreads are quite low, and markets are wide open. So, it makes sense that people take advantage of that today. Those conditions may not prevail late next year.”

The 50-basis points the Fed cut do not change very much the rate a borrower will pay based on SOFR, with several additional points added to incorporate a credit premium. And besides, the issues holding borrowers back go well beyond the interest rate on a loan. As the CFO of another GSIB told analysts,

“I think the 50-basis point reduction is helpful, but not by itself a factor that will drive people to borrow or not. I think they will need to see that come down more meaningfully if that's like the driving force. The uncertainty around the election, the uncertainty around the macro backdrop, I think as people get more confidence that the baseline case of a soft landing will materialize, you get past the election, you see rates come down a little bit. I think all those things will come together and help give clients more confidence about either building inventories or making further capital expenditures that they're holding off on now.”

Lending will pick up faster as rates come down, according to the CFO of a large regional bank in the northeast,

“As rates come down, a lot of folks will be willing to transact and borrow… it's starting to build. But the dam has not broken yet…I think we'll see that trend continue to move up. “

Figure 2: Commercial and Industrial Loan Growth

CECL has nothing to do with lending. Even the level of interest rates is not the most crucial reason why lending growth has been weak. As the president and CEO of a small regional bank in the southeast told analysts, interest rates are normal,

“There's this narrative…that when the Fed started raising rates that oh, my gosh, we're in these high interest rates and then that bled into borrowers aren't going to be able to make payments. And when you look at long-term averages, it really hasn't been an interest rate story. It's been a cost story that has had a dampening effect on companies borrowing money, in building projects and investing in capital goods…it's important for all of us to remember that we're operating in a very normal interest rate environment.”

Green shoots are sprouting in the loan department, according to the CEO of a regional bank in the southeast,

“I would say demand is still a bit tepid, but there's green shoots of progress out there. Our commercial banking pipelines are beginning to build. It is too early to know the timing of when people begin to feel a little bit better. But I suspect we'll need to get the election behind us and maybe a little more demonstration of rate movement downward by the Federal Reserve to see the projects on the fence finally tip over to get executed. But the pipeline is building.”

But the chairman and CEO of a large regional bank on the east coast was not so sure. Maybe this time is different and borrowers are not borrowing because they just do not need the money,

“People just are not using working capital the way they used to. And maybe that's the way they run the company post Covid. Maybe that's the uncertainty that's going to play out over time…I just don't know the answer.”

Yes. Borrowers do not need the money and manage money differently since Covid, according to the chairman and CEO of a large regional bank in the Midwest,

“You just have supply significantly exceeding demand…There hasn't been a lot of investment in CapEx…The next thing is utilization. Everyone basically went long on inventory during the pandemic because there was a lot of inflation and there were supply chain issues…I think there's just been a fundamental adjustment.”

CECL Changed the Credit Cycle

CECL has changed the nature of credit cycles. Far from impeding lending, CECL positioned the banking industry to remain a reliable source of funding for its customers, as its credit reserves already cover expected credit losses on all of its funded exposures for the entire credit cycle. There is even a chance that the reserves are too high for some banks, given the actual losses they have experienced compared to the credit losses they expected. Explaining why his bank might lower reserves, the chairman and CEO of a large regional bank in the Midwest told analysts that three factors have been driving his bank’s CECL reserves,

“There's really three things that, that drive these. One is your view of the macro. And you obviously have a perspective on that. The next is idiosyncratic. And obviously if we were aware of idiosyncratic things, we would…be moving on those. And the third element is the size of the book…Where should the reserve be? We'll continue to evaluate it.”

Running the analysis of a credit exposure over the life of a loan reduces the chances of surprise, which were a feature of previous credit cycles when reserves only captured credit losses that were probable and estimable over the next 24 months. Thus, as the president and CEO of another GSIB told analysts, office lending may have gotten worse, but that was no surprise,

“Things aren't getting better. I’d say it’s more of the same but it's impacting more properties. Maybe to some extent, there is a little bit of contagion to properties that are well-leased.”

Mark-to-Market Accounting and the Underwater, Low-Yielding, Assets Weighing Down Balance Sheets

There have been a lot of surprises in the world of bank treasury. As the chairman and CEO of one of the GSIBs said this month, there will always be surprises, and it would be a surprise if there were no more surprises.

“My view is it is going to happen again. I can't tell you exactly when, but I'd be surprised if it doesn't happen again.”

Mark-to-market has been a longstanding topic in this newsletter, with several chapters that precede the present disaster and even predate the launch of this newsletter. When we launched the newsletter, Statement of Financial Accounting Standard Number 115, the Fed’s decision to require banks to exclude AOCI in regulatory capital, and the FASB’s subsequent decision to let banks move bonds from Held-to-Maturity (HTM) into AFS were a decade in the past.

The new issue in October 2004 was an accounting rule called Emerging Issues Task Force )EITF) 03-01 that was written in a way that caused a lot of confusion among auditors. The rule mandated that bank treasurers incur an Other Than Temporary Impairment (OTTI), a permanent write-down of the portfolio even if no bonds were sold and losses realized. Some auditors interpreted EITF 03-01 to mean that bank treasurers could taint their entire AFS portfolio and that they would incur an OTTI if they sold an underwater bond.

In the middle of the GFC, EITF 03-01 was amended and effectively repealed. However, mark-to-market just evolved into a new potential threat for bank treasurers, when Basel 3 capital rules that came after the GFC forced banks with total assets over $50 billion to include AOCI in regulatory capital. Eventually, that threshold was upped to $250 billion in total assets when the rule was finalized, but banks below that threshold had to choose to opt out of including AOCI in regulatory capital. That rule went into effect in 2015. Now, the new Basel 3 Endgame rules would lower that threshold to $100 billion in total assets, and banks with total assets over that level would be required to include AOCI in regulatory capital.

Regulations are constantly changing. Our staff writers have seen it all, but never in 20 years have they seen the challenges created by their underwater earning assets, complicated by the collision of GAAP, regulatory capital rules, and the Fed’s monetary policy. Mortgage rates edged up since the beginning of this month, effectively shutting the door for bank treasurers who might be searching for opportunities to restructure their bond portfolios, at least for now. As bad as bond portfolio prices got in the early 1990s when the Fed raised rates and caused banks losses in their bond portfolios, nothing has ever been this bad.

Many bank treasurers just have to hold on until the low yielding bonds they bought run off. On the bright side, as the CFO of one GSIB said, as new assets roll on, the yield on the balance sheet will improve. Provided you can wait,

“Not a great deal of change, or us in terms of the securities portfolio from what we said before. Obviously, the HTM continues to run off. I think it's now 13 quarters in a row…which allows us to reinvest at higher yields. So that remains basically our -- first off with respect to the investment strategy is just below that to continue rolling down…We're normally putting that into cash and cash equivalents or we're paying down expensive short-term liabilities…we're taking a little bit of one- to three-year fixed rate in the last couple of quarters.”

Most of his portfolio is in the HTM and cannot be restructured, and the bonds in AFS are mostly swapped, he explained, so there really is not much that can be done but wait until the bank’s low-yielding assets run off.

“At this stage, we don't see any need for that. Remember, most of our securities in the available for sale, we've got those swapped to floating.”

Bank treasurers who have had the cash and the capital to sell what low-yielding bonds they could last quarter when the 10-year Treasury established a solid range under 4% are already reaping the benefits this quarter as their higher-yielding assets generate NIM for the bank. Looking back on the trade he did last quarter, the CFO of a large regional bank in the Midwest explained that his primary motivation for the bond restructuring was to improve liquidity.

“It was just an opportunity…to improve our liquidity profile as well as some lower yielding securities that have seasoned to reposition those.”

Many banks today cannot afford to ride out their underwater assets until they run off and cannot afford to restructure. Their outlook is not good, dare we say grim. Even selling the bank will be painful to shareholders when they see the bid, the president and CEO of a community bank in the southeast that has managed the acquisition of other banks told analysts,

“What I call the zombie banks, who are stuck with AOCI issues, not just in their securities portfolio, but also in the loan rate interest rate mark...Some of these banks may have been using hope as a strategy for interest rates falling and unwinding some of that AOCI. But I think the reality has hit in many places…just look at the 10-year, still around 4%...some of these banks have, I think, come to realize that it's a slower boat to China to unwinding some of these marks than they expected.”

If there are bank treasurers who are lucky enough to be sitting with some extra cash at the Fed overnight, their question right now is whether to continue sitting there or move some money into bonds. The back end of the yield curve moved higher in the last few weeks and made the yield curve less inverted. In the previous month, the 3-month-5-year spread flattened from negative 160 to negative 70 basis points. Mortgage products also got more attractive as an investment idea than a month ago, as the 2s-10s spread steepened, and the curve turned positive by a dozen basis points.

Bank Deposit Franchises Have Never Been Stronger Than They Are Today

Yield curves are connected to deposit franchise valuation. Most bank treasurers agree that positively sloped yield curves are consistent with a bank’s ability to extract value from deposits tied to short-term rates in earning assets tied to intermediate rates. The chairman and CEO of a large regional bank on the East Coast explained the basic math behind a positive sloped yield curve,

“Zero cost deposits are worth a lot if there's any slope to the curve, we get that benefit with our fixed-rate assets…All else equal, if we end up in an environment where front rates are three and change and back rates are somewhat higher than that, that's the really attractive environment for banks.”

All else equal, a positive slope is how bank treasurers make money from their deposits, as explained by the CFO of a GSIB. Still, the pace of the rate cuts also matters, especially for asset-sensitive banks, which might hold a lot of deposits that are either at 0% in a checking account or not immediately repriceable. If rates come down too fast, NIMs will suffer, he explained,

“All else being equal, a steeper curve is better for us. But I think what I would also say is that this…is disproportionately in the front end. We want a steeper curve. But having the Fed cut more than what's currently in the yield curve is…at the margin…a headwind for us. We remain asset sensitive to Fed cuts.”

However, according to the chairman, president, and CEO at another GSIB, all this focus on deposit betas for asset-sensitive banks is beside the point. The spread between the effective Fed funds rate and the cost of funding (Figure 3), including both noninterest and interest-bearing deposits, has never been higher. Bank treasurers could not hope for a better operating environment to make NII.

Figure 3: Effective Fed Funds Rate Less Cost of Funding, All Commercial Banks

Even without the benefit of noninterest-bearing deposit funding in the cost mix, bank treasury has still never seen better days, at least for a long time, he explained,

“There has been much discussion over the last couple of years about betas. But if you look at where we stand at the end of the third quarter, the difference between Fed funds and the total interest-bearing cost of our deposits is around 250, almost 260 basis points. If you think -- if you look at quarter two in '19, when the Fed funds hit the highest rate in the last cycle, that difference was 160 basis points, 170 basis points…When the Fed's funds rate was in the 2.75 to 3.25 range, this industry was able to make more money.”

What We Have Learned

What have we learned from talking to bank treasurers over 20 years of writing this newsletter? Plenty. We have learned that bank treasurers want to manage interest rate risk, not avoid interest rate risk, which means trying to steer between too much and too little. They struggle to estimate that risk, just as the Fed struggles with figuring out where the neutral interest rate might be at any one time. It is next to impossible to manage interest rate risk and monetary policy when markets and the economy move a lot. Volatility works against transparency.

We also learned that bank treasurers have no more insight about the direction of interest rates than anyone else, do not get a bump in their bonus checks each year for taking on risk, and get a lot of blame when it does not turn out well, as is now the case, blamed as they are for putting on the assets that are presently so underwater. A bank treasurer combines asset manager and trader, all rolled up into one. They want to buy low and sell high but have to consider liquidity, asset-liability management, and risk-return. Because they know that not every profitable trade is a good fit, the best bank treasurers can manage that balancing act.

So, that is one thing. And because of that, bank treasurers tend to revert to what they know. They are not about swinging for a home run. Bank treasurers do not necessarily care about expanding NIMs as much as managing stable NIMs. Bank treasurers are all about stability, another reason today’s volatile market makes them uneasy. Thus, the CFO of a regional bank in the northeast was happy to report a stable NIM outlook for 2025, even if that was not official guidance,

“We think we're at a stable NIM. We may be plus or minus 3 basis points as we move forward, but that's the range we're looking at going forward in the '25.”

We have learned over the years that a bank treasurer is no magician. Bank treasurers cannot fix a balance sheet with underwater fixed-rate assets and expensive funding, at least not immediately or without some major costly balance sheet restructuring. It is also true that a high-yielding bond portfolio cannot make up for a low-yielding loan book and drive earnings. You need loan growth for earnings growth, as the CFO of a regional bank based in the southeast told analysts,

“The missing ingredient really for us to continue NIM expansion and NII expansion in a down rate environment really needs to be balance sheet growth…we're focused on growing the loan book into next year. So, if we're successful in doing that, we certainly have, I think, a pretty good chance as a modestly asset-sensitive company, being able to continue NIM expansion in a down rate environment.”

The other thing we have learned from interviewing bank treasurers over the years is that regulations are a fact of life in the world of bank treasury. However, bank treasurers do not need the rules to manage their bank’s balance sheet conservatively, efficiently, and profitably. Regulations requiring them to run liquidity stress testing and maintain liquidity coverage ratios (LCRs) are the bare minimum that bank treasurers who do their job well take seriously and always do.

They do not need a bank examiner to tell them what thresholds they must maintain, which they always strive to exceed. They long ago got the joke that regulations are just a way for regulators to blame them when something goes wrong. (“Oh, if only you followed an LCR, or if only you did the stress test, or held more capital.”) There is always a reason to tighten regulations following a crisis, even if the remedy has nothing obvious to do with the problem that caused the crisis.

We learned that liquidity risk can be more complex than interest rate risk. Liquidity should be ample. Reserve balances have not budged since QT began, yet there was a significant spike in SOFR that is still difficult to explain. Liquidity is mysterious. There is plenty of liquidity, and then suddenly, there is none. This is why bank treasurers will remain in cash, even if it is expensive.

Finally, we learned that this time is different because every time is different. But this time is different. We have never seen fiscal stimulus during Covid in as concentrated a time frame as we saw, and even as the pandemic has faded mainly along with work-from-home arrangements, the consumers driving the economy are still consuming.

Consumers have blown through the surplus in their bank accounts. But that stimulus is still coursing through the economy, sitting in a retailer’s account, or has gone elsewhere. It does not matter. Like jet fuel poured into a car’s gas tank, the Covid stimulus is still driving economic growth to a degree not seen since the U.S. spent 40% of its GDP to fight WW2 and pulled itself out of the Great Depression.

There is a lot of uncertainty in the world of bank treasury today, but frankly, this is just the norm, given all the moving parts that bank treasurers need to watch and contend with. Something is always coming up. A spike in SOFR, rate cuts, inverted yield curves, weak loan demand, negative AOCI, deposit betas, new regulations, the latest accounting rule, and so on. Bank treasurers have a lot on their plate, and our editorial staff try to cover it all. We look forward to continuing the effort and seeing you all again next month for another edition of The Bank Treasury Newsletter.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2024, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

Real GDP growth fell to 3% through the first half of 2024 (Slide 1), and business lending remained soft (Slide 2) as bank treasurers hope that the Fed’s rate cuts spur a rebound in credit expansion. Over the last 12 months, commercial banks increased total loans by $0.3 trillion to $12.5 trillion, and investment securities by $0.2 trillion to $5.3 trillion (Slide 3). On the other side of the balance sheet, the rebound in deposits since the summer flattened, while savers shifted into money market funds, which hit a record $6.9 trillion last month (Slide 4).

Bank treasurers took advantage of the rally in fixed income in Q3 2024 to restructure their bond portfolios, selling securities and using the proceeds to reduce wholesale funding. Thus, the financial industry reduced its Bank Term Funding Program (BTFP) liabilities, to less than $60 billion from $170 billion where it peaked last April (Slide 5). Reserve deposits at $3.2 trillion are unchanged since Quantitative Tightening began in June 2022, and the U.S. Global Systemic Important Banks (GSIB) account for more than half of the balance of reserves held by domestic banks (Slide 6).

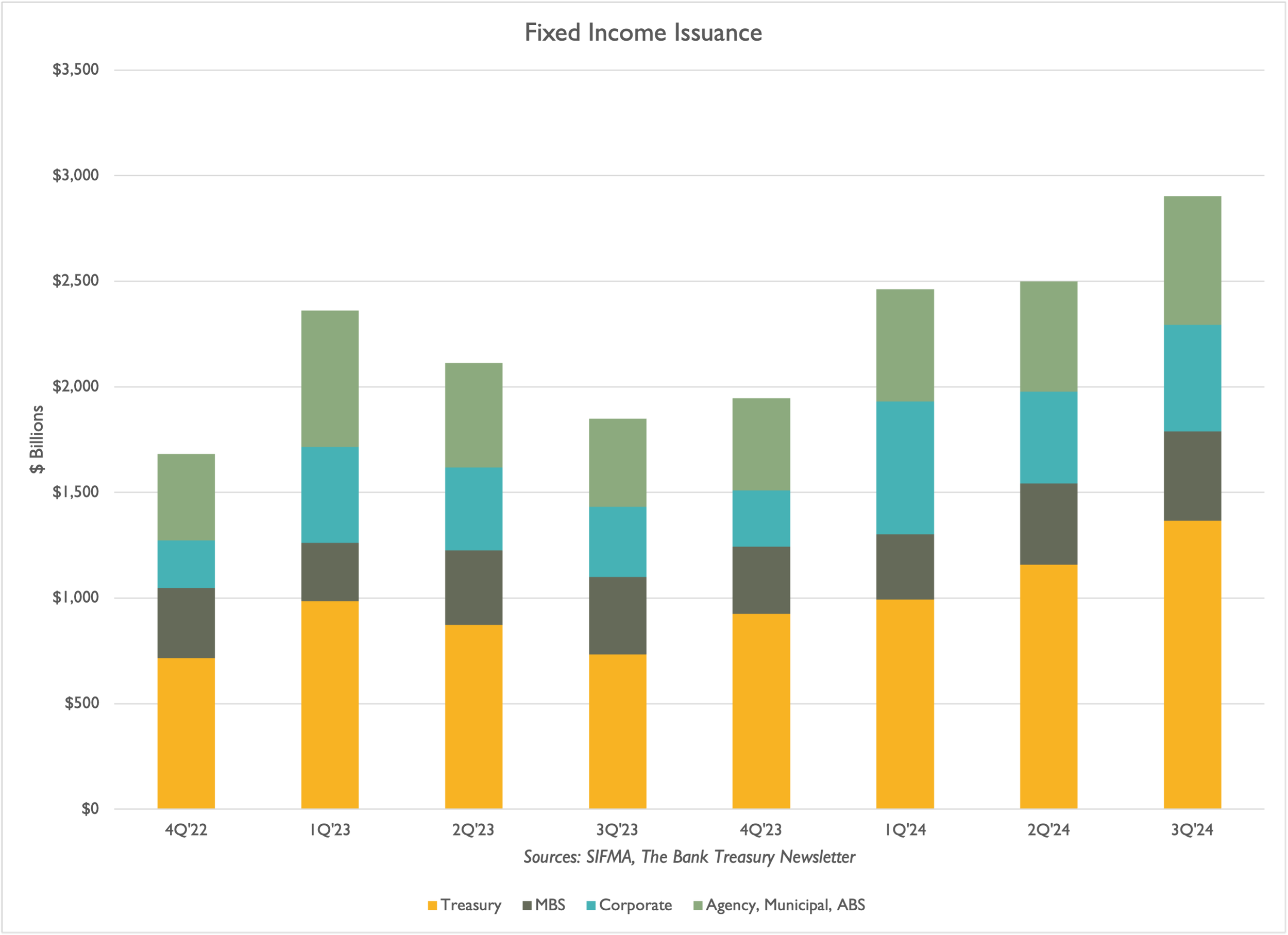

The Treasury’s stepped-up issuance calendar this year (Slide 7) drove fixed-income securities outstandings (excluding mortgage-backed securities) to a record $45 trillion, with Treasurys reaching $27 trillion through the end of September (Slide 8). Over month-end, the Secured Overnight Financing Rate (SOFR) jumped by 21 basis points, to 5.05% on October 1, before settling back to 4,83%. This was the most significant surge in the rate since September 15 and 16, 2019, when the rate jumped by over 305 basis points to 5.25%.

Some money market participants believe that Treasury issuance has put pressure on primary dealer balance sheets and may have caused the spike in SOFR. There are signs of pressure as primary dealer net positions in Treasurys peaked in September (Slide 9) at over $230 billion. In addition, sponsored repo and reverse repo volumes with hedge funds temporarily spiked up over month-end, from $1.5 trillion to $1.8 trillion (Slide 10).

Real GDP Growth Comes In For A Landing

Business Lending and GDP Growth Since WW2

Banks Grew Bonds and Loans In Lock-Step

Bank Deposits Flatten While Money Markets Surge

Banks Sold Bonds To Pay Down BTFP

GSIBs Held 54% of Total Reserve Deposits

Treasurys Drove Fixed Income Issuance

Treasury Share of Fixed Income Grew

Dealers Cut Treasury Positions Over The Summer

Sponsored Repo Volumes Spiked Over Month-End